Q1 2026 produced a Global funding of $300 billion, where AI took four-fifths of every dollar, and a Series A founder outside AI faced the same tough market as in 2025.

Close to $297 billion was deployed in about 6,000 startups, an all-time quarterly high that grew roughly 150% both quarter over quarter and year over year, and close to 70% of everything venture investors spent in all of 2025[1]

AI took 81% of that capital, and a single tier of frontier labs absorbed most of it[1]. Underneath the megadeals, seed deal counts fell, the United States IPO market stayed slow through a software selloff, and limited partners routed most new commitments to a handful of large firms.

Investors are asking the same questions:

Is this an AI bubble and will it burst in 2026?

Are OpenAI and Anthropic's valuations real?

Why can a non-AI founder no longer raise a seed round?

Can an emerging manager still close a fund?

When does the IPO window reopen?

Each F1GMAT Premium Quarter 1 2026 trend analysis below answers these questions.

Contents

- Key Data for Q1 2026 VC Trends

- Key Observations

- Skills in Demand: Venture Capital Q1 2026 Industry Trends

- Venture Capital Industry Trend Q1 2026 #1: AI Took Four-Fifths of Every Venture Dollar, and the Bubble Question Got Louder

- Venture Capital Industry Trend Q1 2026 #2: Record Capital Concentration – 5 VC Firms Won it All

- Venture Capital Industry Trend Q1 2026 #3: Stress Test for the AI Boom with SpaceX IPO

- Venture Capital Industry Trend Q1 2026 #4:Venture Moved Into the Physical World

- What to watch in Q2 2026

Key Data for Q1 2026 VC Trends

| Venture Capital indicator | Q1 2026 figure, and what it means |

|---|---|

| Global venture funding (Crunchbase) | $297B invested across about 6,000 startups, up roughly 150% on both the prior quarter and the prior year, which packed close to 70% of all of 2025's venture spending into a single quarter, the largest venture quarter ever recorded[1] |

| AI's share of all funding | 81% ($239B) of every venture dollar went to AI companies, up from 55% a year earlier, the highest concentration of capital in one sector that venture has on record[1] |

| The largest rounds | The four largest rounds reached $188B (OpenAI $122B, Anthropic $30B, xAI $20B, Waymo $16B); adding Databricks ($7B) the top five hit $195.6B, about three-quarters of all US deal value[2][1] |

| US deal value, and the market without the giants | $267.2B in total, but strip out the five biggest deals, and it drops 73.2%, which is the far smaller market an ordinary founder actually raised in[2] |

| Late-stage funding | $244B across 582 deals, up 203% year over year, as investors paid up for proven, later-stage companies over new ones[1] |

| Seed dollars versus seed deals | $12B, up 30% in dollars, yet the number of seed deals fell 31% to 3,700, so more money reached fewer founders[1] |

| LP money to the top five firms | 73.1% of all the cash that investors committed to venture funds went to just five firms, and Andreessen Horowitz's January fund alone was over 18% of all 2025 US commitments[7] |

| US exit value, and the cash without the giants | $347.3B, a record, but remove the five largest exits and the total fund raised falls 86.6%. The real return on cash was low for most funds [2] |

| DPI, cash returned to fund investors (2017 funds) | 0.27x, about 27 cents back for every dollar committed roughly eight years in, near the lows last seen after the 2008 crisis[14] |

| United States share of global VC | 83% ($247B), up from 71%, so the US took a larger slice of a much bigger pool while other regions shrank in relative terms[1] |

Key Observations

The estimation on the deal size for Q1 2026 varies depending on who you are asking.

KPMG counted $330.9 billion across 8,464 deals, Crunchbase counted about $297 billion across 6,000 startups, and CB Insights counted $286 billion[1][7]

The confusion arises because no one knows how to classify the large checks that sovereign-wealth funds and private-equity-style investors wrote into AI labs

Are these venture capital funds or private credit?

When PitchBook-NVCA removed the five largest deals, United States deal value fell 73.2% and exit value fell 86.6%[2]. In plain terms, take out a handful of giant transactions and the record quarter becomes an ordinary one, which is the market reality a typical founder or fund is dealing with.

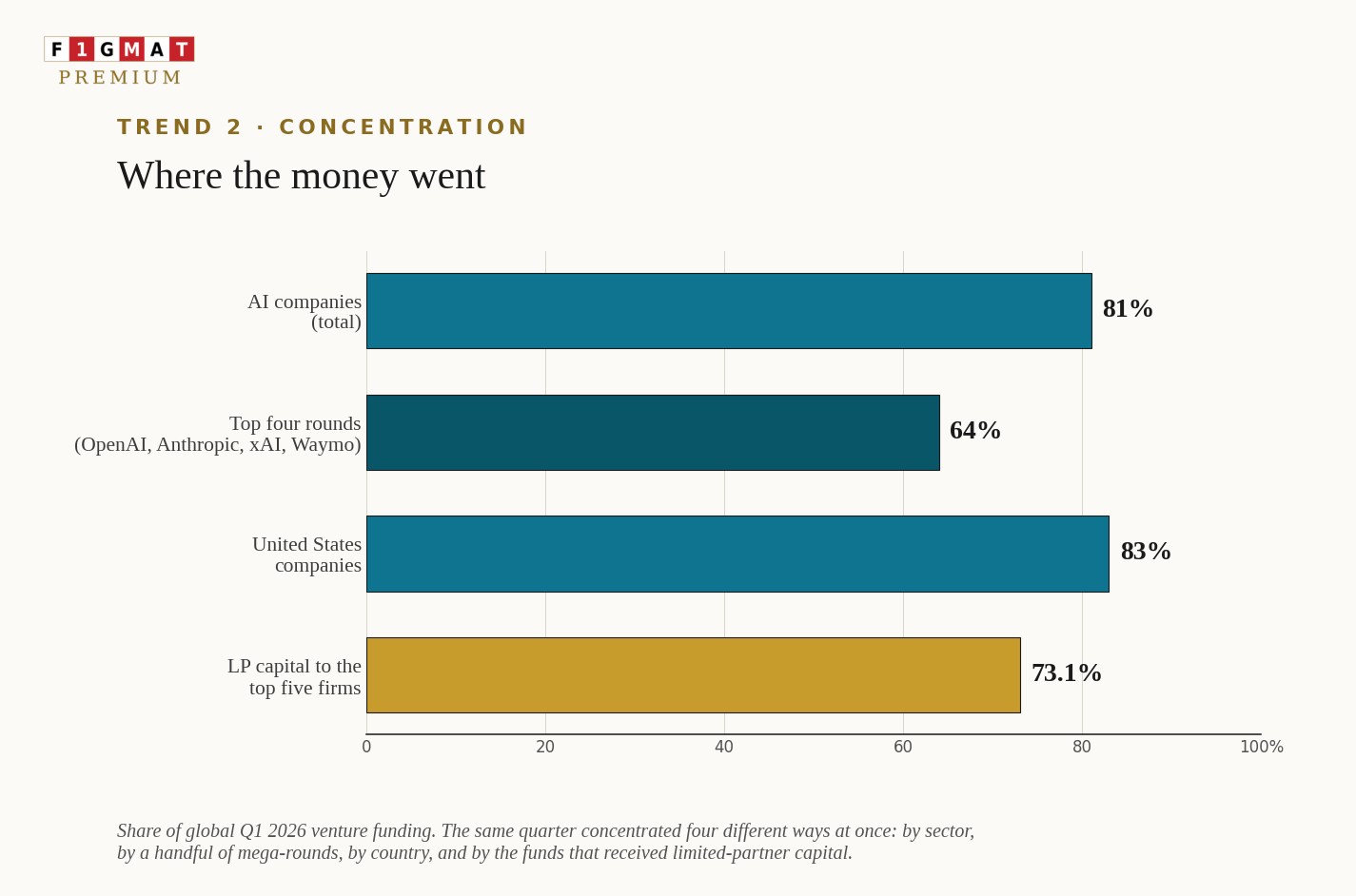

Four companies (OpenAI, Anthropic, xAI, and Waymo) captured 64% of global dollars, United States companies dominated 83% of the global total, and just five venture firms took 73.1% of all the money that investors committed to new funds[1][7]

The high concentration of VC fund in three categories - by company, by country, and by fund all happened in the same three months.

DPI, the measure of how much cash a fund has actually paid back to the investors in it, was near 0.27x for 2017-era funds.

Only about a quarter of the committed money had come back roughly eight years in, and some universities sold their fund stakes at a discount to raise cash[14][8]. That is why fund investors are now asking to see real distributions before committing again.

The AI bubble question?

Benchmark's Bill Gurley said a reset is coming. The International Monetary Fund said a burst is possible but smaller than what we saw in 2008. And several venture partners quoted 2026 as the year AI buyers will start paying for results instead of its potential[13][12].

The disagreement is about price and timing, not about whether the technology is real.

Within AI, the fund allocation traced the shape of an arrow across the technology "stack."

The arrowhead was the expensive bottom (chips, data centers, and the AI models themselves), where the largest dollars concentrated. The fletching was the crowded application layer at the top, where capital fanned out thinly. The long shaft between them was the middle layer that makes AI usable in practice (a company's own data, memory, testing, and governance), which stayed starved - the layer Bessemer named as the place value shifts once models become cheap and interchangeable.

Skills in Demand: Venture Capital Q1 2026 Industry Trends

| Role (and what it does) | What the Q1 2026 market now requires |

|---|---|

Investor / Partner decides large fund allocation | Value an AI-lab round against the cost of computing power and electricity, read the fine print that inflates a headline valuation (ratchets, IPO protection, revenue guarantees, all defined later in this report), and tell a reported valuation apart from the real economic value of the shares. |

Early-stage / Seed writes a startup's first institutional check | Choose well when there are fewer deals but bigger rounds, so a single pick can decide the fund's return, and judge whether a young company can defend itself against far better-funded AI labs. |

Growth / Late-stage backs larger, more mature companies | Underwrite capital-heavy "physical AI" businesses such as robots, self-driving fleets, and data centers, where the economics look nothing like software and the costs run more like a utility. |

Fund manager / General Partner raises and runs the fund itself | Raise money in a market where five firms take most of it, which means showing a specific, legible edge and a credible plan to return cash to investors. |

Liquidity / Portfolio operations gets money back out of investments | Engineer exits through acquisitions, secondary sales, continuation funds, and foreign listings while the United States IPO market stays mostly shut. |

We observed four forces shaping the quarter.

Venture Capital Industry Trend Q1 2026 #1: AI Took Four-Fifths of Every Venture Dollar, and the Bubble Question Got Louder

Artificial intelligence companies raised $239 billion in Q1 2026, which Crunchbase put at 81% of all global venture funding for the quarter, up from 55% a year earlier[1]

PitchBook measured the same wave from its own dataset and reported $255.5 billion of AI venture funding, a figure that passed the entire full-year 2025 AI total of $254.4 billion[3]. The scale of the fund inflow has brought back the AI bubble question.

Is AI in a bubble, and will it burst in 2026?

Benchmark's Bill Gurley said in March 2026 that the AI trade is about to break and that a reset is coming[13]. The International Monetary Fund took a middle position, warning that a burst is possible while judging that it would not match the 2008 financial crisis in systemic damage[12]. Several venture partners surveyed by Fortune framed 2026 as the year the standard changes. Redpoint's Meera Clark and Vanta's Stevie Case both said buyers will pay for AI that raises revenue or automates real work [12].

Roughly $200 billion deployed into AI in a single year has to produce several trillion-dollar outcomes within five years, which is an ROI target that seem impossible as a similar investments take decades to earn any return[12].

645 Ventures' Nnamdi Okike expects the reckoning to begin by the end of 2026. The valuations will fall both in public and private markets[12].

For a fund, the risk window is the 2026 to 2027 earnings cycle.

The AI bubble debate, Q1 2026

| View | Named source | Core claim |

|---|---|---|

| Reset is near | Bill Gurley, Benchmark[13] | The AI trade is about to break and a reset is coming. |

| Possible, not catastrophic | IMF[12] | A burst is possible but unlikely to match 2008 in systemic scale. |

| ROI test, not a pop | Meera Clark, Redpoint; Stevie Case, Vanta[12] | 2026 is the year buyers pay for measured value, not promise. |

| Markdown by 2027 | Nnamdi Okike, 645 Ventures[12] | Capital shifts away from spend-at-all-costs; valuations fall in 2027. |

| Time compression is the tell | John Kim, Sendbird[12] | $200B a year must produce trillion-dollar outcomes in five years. |

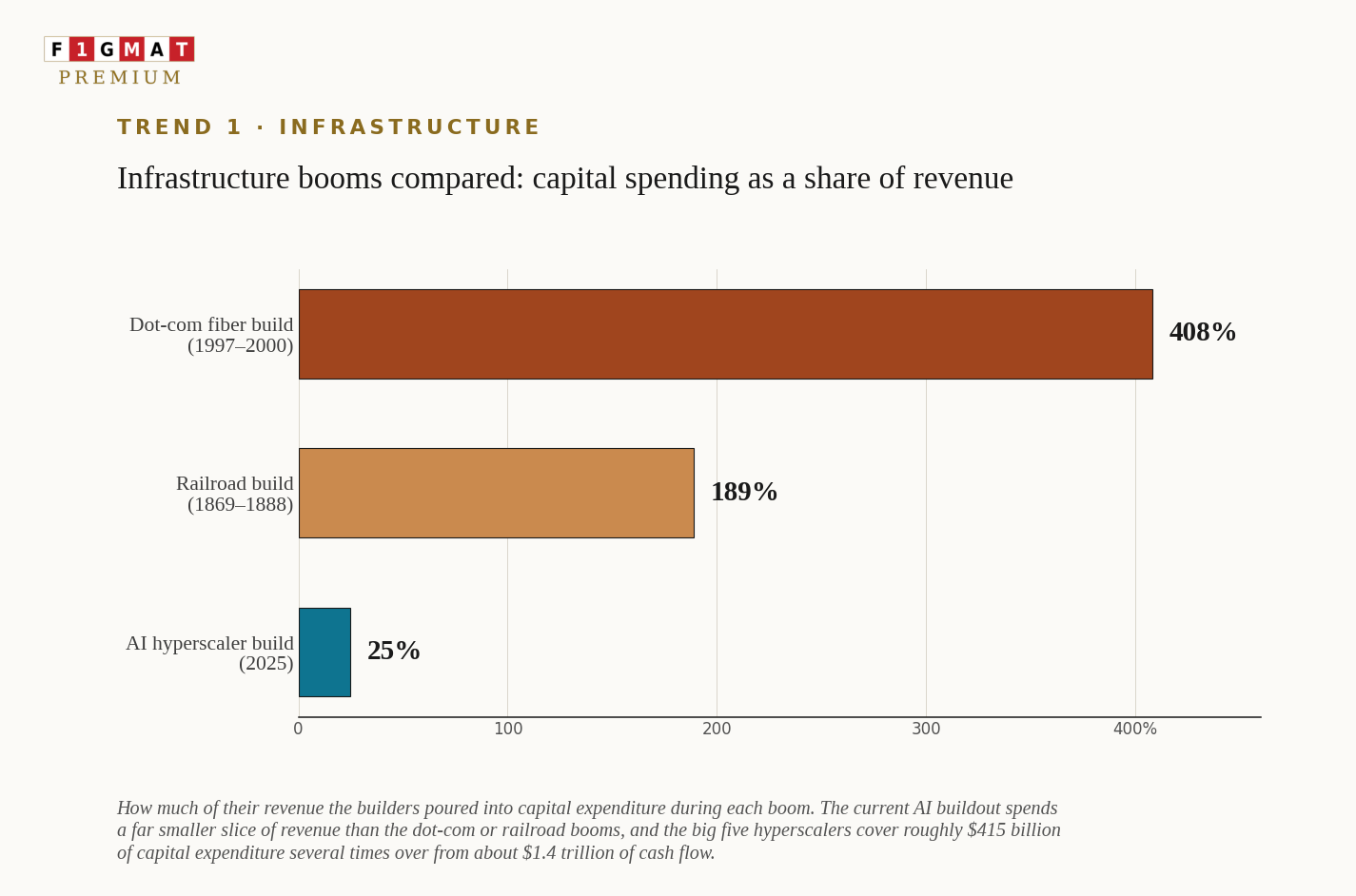

Infrastructure Boom – A historical Perspective

Ropes & Gray, citing Blackstone, set the current infrastructure buildout against the two classic infrastructure manias – Dot-com Fiber Buildout from 1997-2000 and the Railroad Buildout from 1869 to 1888 and found it far less stretched on capital expenditure as a share of revenue [56]

The 1869 to 1888 railroad build laid the physical network of the American economy and still ended in repeated panics and bankruptcies. The pattern continued over a 100 years later from 1997 to 2000 when the dot-com bubble wired the internet and still wiped out most of the companies that financed it.

A real and lasting infrastructure and a brutal investor loss are not mutually exclusive.

The difference in Q1 2026 is that the big five hyperscalers are funding roughly $415 billion of capital expenditure against about $1.4 trillion of operating cash flow [56]

The risk is in demand.

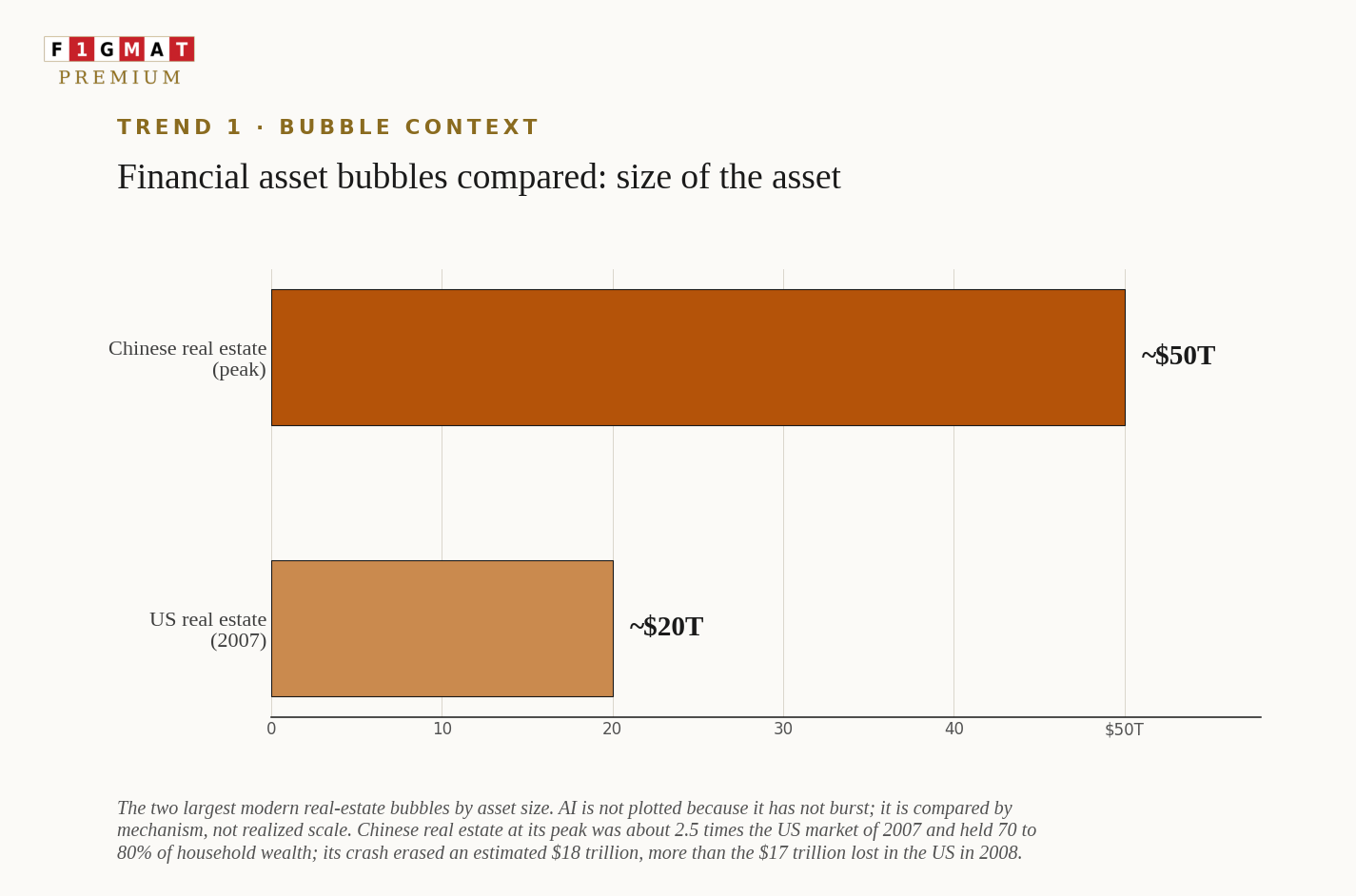

Is it a financial asset bubble? Like the 2008 Sub-Prime or the China property Bubble

A financial asset bubble is the closest to the phenomenon we are seeing in AI, because it has all the ingredients of the previous 2008 sub-prime crisis - an asset appreciates and draws speculation, supply expands until it outruns genuine demand.

The regulatory conditions are loosened to keep the volume growing.

Financial engineering is employed on top of loose regulation to redistribute fund and disguise the risk.

Hidden leverage builds, and a trigger sets off the cascade.

The 2008 subprime crisis is the textbook case.

United States house prices rose, demand was met and then exceeded, lending standards were dropped (subprime, no-documentation, and teaser-rate loans) to keep originating, and the loans were packaged into mortgage-backed securities, collateralized debt obligations, and credit-default swaps that sliced and sold the risk until the leverage was hidden across the banking system.

When prices fell large banks required bailouts[12].

Bubbles are not a United States phenomenon.

Anatomy of a financial asset bubble: China property Bubble

China's property bubble is the larger modern example.

By 2020, real estate and its upstream and downstream industries reached about 25% to 30% of China's GDP and held 70% to 80% of household wealth, which made Chinese real estate roughly a $50 trillion asset class, about 2.5 times the size of the United States real estate market in 2007[58][59]

Developers such as Evergrande pre-sold unbuilt apartments and used the new deposits to finish earlier projects, a presale model in which new money covered old obligations, and they layered on developer bonds and wealth-management products instead of Western-style derivatives[58]

When regulators capped the leverage developer was using, sales stalled and Evergrande defaulted on more than $300 billion of liabilities. Barclays estimated the crash erased about $18 trillion of household wealth from 2021 onward, exceeding the inflation-adjusted $17 trillion lost in the United States in 2008[60]

The difference from the 2008 sub-prime crisis is that China carried less hidden derivative leverage than the United States but a far larger asset at stake, which is why its unwind has been slow and managed well rather than a single 2008-style seizure[58].

| Stage | US subprime, 2008 | China real estate, 2021 | AI, 2026 |

|---|---|---|---|

| The asset | Houses and the mortgage bonds built on them | Apartments, much of it pre-sold before being built | Private AI companies and the compute behind them |

| What drove demand | Cheap credit and faith that prices only rise | Urbanization, with capital controls making property the main savings vehicle | A general-purpose technology and the fear of missing the winner |

| How conditions loosened | Lending standards dropped: subprime, no-doc, teaser rates | Developers pre-sold unbuilt units and piled on leverage to fund prior projects | Looser diligence, structured terms, and circular or vendor financing |

| Engineering layered on top | MBS, CDOs, and CDS sliced and sold the risk | Developer bonds and wealth-management products; fewer derivatives | Circular deals, structured equity terms, private credit, and asset-backed compute leases |

| Where leverage hid | Across the banking system and households | In developers and local governments | Low at the center, rising at the leveraged edge |

| Realized outcome | About $17T household wealth lost; global crisis and bailouts | About $18T household wealth erased; slow, managed unwind | Not yet; still at the conditions-loosening stage |

The counter-counterpoint is that the cost of the infrastructure is falling, with Alphabet reporting its Gemini server unit costs fell 78% over 2025[56]. But converging capability and collapsing cost are exactly what erodes the pricing power of the model layer, which is the risk that investors must understand other than the risk from falling demand.

Is Anthropic's valuations real?

PitchBook-NVCA flagged that some frontier-lab valuations carry structured features that overvalues the business without a matching change in the business[2]

Anthropic illustrates the speed of the repricing. It raised at roughly a $380 billion post-money valuation in Q1 and saw that figure move toward $965 billion within two to three months, a near-tripling that PitchBook-NVCA itself said should be questioned [7].

The magic rise in valuation happens because of protections.

Let us say one investor agrees to pay $100 a share and there are 5 billion shares, the company is "worth" $500 billion. The valuation is only as real as the investor agreed to pay.

Now bring in protection.

First with ratchet protection, where if an investor pays a high price now, let us say $100. If the company raises the next fund at lower valuation, let us say $80, the $20 difference is compensated from the shares of the founders and employees.

Square's 2015 IPO is a case study on the worst form of ratchet protection where the late investors had a ratchet protection into IPO and when the listed price was lower, the company had to create millions of shares, diluting the value of the stock further.

Second with IPO downside protection. If the company goes public below an agreed price, the investor gets a guaranteed minimum return or a top-up of shares to match the investment. So a sovereign fund will sign off on a giant private valuation partly because it has a price floor underneath it. If the public market later pays less, the fund still gets its money back and the common stock holders lose the stock value.

For AI’s case, there is a third protection called revenue guarantee where the large investors into the model companies are also their biggest customer. A chipmaker or cloudprovider will subscribe to the model in return to purchase the investor’s products or services. As revenue on paper increases, valuation also increase.

When Anthropic's valuation increased from $380 billion to $965 billion in a quarter, the right question is not whether the business tripled, it is how much of that $965 billion is a real price and how much is the protected price a handful of insured investors were willing to sign, with the common shareholders paying the gap in valuation.

Reporting collated through the quarter put Anthropic's annualized run-rate near $30 billion and OpenAI's near $25 billion, with PitchBook-NVCA estimating that SpaceX, OpenAI, and Anthropic together could generate close to $2.5 trillion of value over time[7].

Following the money down the stack: chips, models, and the layer in between

The chips layer’s concentrated value stayed mostly out of venture’s reach.

Nvidia holds the general-purpose GPU position, custom accelerators from the hyperscalers are co-designed by Broadcom and Marvell, and almost every advanced chip is fabricated by TSMC and printed on an ASML machine.

The hardware assets is owned by a few public mega-caps and a few sovereign-backed players[16].

The model layer took the megarounds, with OpenAI, Anthropic, and xAI absorbing the bulk of the $239 billion AI total[1].

The compute layer between them, the data centers and the supercomputers, pulled in CAPEX at an industrial scale, with xAI's Colossus cluster alone cost about $10 billion[17].

The application layer at the top drew the most companies and the most attention, and a far more sober reality.

Most founders outside the frontier-lab category in the application market had deal counts at their lowest since 2018 even as average check size doubled[3].

Implication for the VC professional

The only call that matters in an AI round is defensibility, whether the company can hold its lead for more than two quarters when the same capital funding it also funds its rivals. Most cannot, which is why the contrarian move is to back the starved middle of the stack (data, memory, evaluation, governance) rather than frontier-lab equity priced at the layer most exposed to commoditization.

For aspiring VC and MBA applicants

For aspiring VC and MBA applicants, ignore the AI a bubble question and learn to place a company in the right AI stack from chip to energy to application layer. Based on this classifying you build the entire strategy.

Venture Capital Industry Trend Q1 2026 #2: Record Capital Concentration – 5 VC Firms Won it All

The quarter's total fund raised was a new record.

Crunchbase counted close to $297 billion invested, and PitchBook-NVCA put United States deal value at $267.2 billion, higher than every full year on record except 2021 and 2025[1][2]. But the records came from a handful of giant deals, and the proof is the gap between the median deal and the average deal size.

At Series A, the median round was $19.6 million against a $39.6 million average, and at Series C it was $75 million against $124.6 million. The typical company raised about half of what the average implies[2] showing that fund raising is a winner take it all phenomenon since the pandemic.

Q1 2026 took it to a new extreme.

Is this a two-tier market?

Yes.

Mega funds lead $5 million seed rounds where a single company can raise three times the required fund in six months. In the non-AI funding ecosystem angel activity has slowed, and most founders find it hard to raise funds[11]. Angels, who often co-invest with or follow VCs naturally tilted their attention toward the in-news narrative. The “spray and pray” of the 2020s where angels and early investors made 20-30 small bets has evolved to thesis based investments.

When a late-stage AI deal is priced at roughly three times the price of comparable non-AI rounds while investors demanded about 2.5 times the growth to justify the valuation[11]. The shift towards thesis-based investments attracted disproportionate funds to Dual-use technology (commercial and defense), deep domain expertise for disrupting vertical software, procurement expertise (govt. software contracts), and any space with hardware-software integration.

Valuations for non-AI companies are now 20-40% below AI peers at the same stage but all the startups are now experiencing higher expectations.

The traction AI leaders gained in the past three years have set aggressive growth targets for all startups.

The changing startup fundraising dynamics have decreased the competition in robotics, defense tech, manufacturing automation, and even in specialized enterprise tools.

Strong teams with real traction can stand out more if they accept the start-up reality. Startups with strong unit economics and clear path to profitability with moat against AI-driven competitors are all earning the checks.

Why the fear from writing checks?

The concentration of funds – late stage and early stage to few AI companies arose through liquidity drought. And this development was not sudden.

Median DPI, distributions to paid-in – the cash a fund has actually returned to its investors for the 2017 vintage fund was about 0.27x in early 2025, near levels of loss last seen after 2008. Even after eight years in, investors had only earned back about 27 cents on each dollar. Funds without exits cannot put their earnings back to the VC and PE funding ecosystem. The IPO market slowing down with the arrival of AI and the valuation collapse of SaaS companies is one reason.

The second reason is the pressure university endowments faced. A large parallel VC ecosystem works in collaboration with university endowments. These funds support the cost of an entrepreneurial candidate in research or a Master’s program, building their startup through the university incubator ecosystem.

When Trump threatened to cut off funding, universities had to aggressively search for liquidity.

Yale found the hard way how wrong valuation can affect even the most stable funds.

Yale endowment, the model David Swensen built, put roughly 60% into illiquid alternatives like venture capital, buyouts, and real estate on the logic that a perpetual fund gets paid a premium for locking money up. The thesis was right and returned 9.5% for a decade on average. But during the 2021-22 technology valuation boom, cheap money pushed Yale's venture investments to its peak. Because the model discouraged liquidity, those holdings froze at stale valuations with no rounds, sales, or IPOs to reprice them. In 2024, the ventures returned only about 3.5% and drag the fund to a 5.7% a year. With gains stuck on paper while the budget pressure from low federal funding pushing for liquidity, Yale was pushed to sell up to $6 billion of private stakes on the secondary market at a discount in 2025, close to 15% of its endowment [14][15]

Why Five Venture Firms Dominate the Entire VC Ecosystem?

Five venture firms captured 73.1% of all limited-partner capital raised in Q1 2026, and Andreessen Horowitz's January 2026 fund alone represented more than 18% of all 2025 United States commitments[7]. The intuitive assumption is that limited partners backed Andreessen Horowitz, Thrive Capital, Founders Fund, Kleiner Perkins, and Battery Ventures because these firms post the best returns, but the disclosed data does not support that. Only Thrive has a hard, recent figure, a 2.4x DPI[61], and it comes from its 2016 fund, a decade old and from the easy-exit era; for the other four, fund-level returns are largely undisclosed, and the raise happened in the weakest fundraising year since 2017, when distributions had dried up across the board.

What the five actually share is access and thesis.

Access runs through four reinforcing channels. First, allocation is rationed.

Frontier labs like OpenAI hand funding rounds to a short, pre-approved list of investors. And a smaller fund cannot buy its way on.

Second, check size limits entry, because only a multibillion-dollar fund can write a $1 billion line, which is why raising a $15 billion fund and reaching the biggest rounds are the part of the same strategic goal.

Third, access compounds, since firms already on the cap table hold pro-rata rights to keep investing. Past access manufactures future access.

Fourth, founders pick investors for the brand, handing marquee firms allocations that capital alone cannot buy.

Thesis as the reason for the five venture firms capturing 73.1% of all LP’s capital in Q1 2026 can be explained through 3 factors.

First, a thesis is a pre-commitment about where the money goes.

For example, a16z's "AI is eating software" is an instruction that routes its $15 billion into AI-focussed infrastructure, apps, and defense ideas before any single company is picked.

The second reason is that a thesis creates the mandate for the team. The mandate becomes the culture. The culture attracts the right founders and VC peers.

Third - each firm offers a distinct bet like Founders Fund on hard tech and defense, Kleiner Perkins on an AI turnaround, and Battery on enterprise AI. This superspecializaation allows LPs to choose a flavor within the same thesis.

How was 2023-25 for Emerging managers?

An emerging manager is a firm raising one of its first funds, roughly Fund I through Fund III, without the long track record an established firm carries. A limited partner, or LP, is the investor that puts money into a venture fund, which can be an endowment, a family office, a pension, or a wealthy individual’s fund.

Redbud VC called 2023 to 2025 the worst three-year stretch for emerging managers in modern venture history, noting they captured only 23% of all fund value in 2024, a decade low[9].

VC Lab's data, drawn from the emerging-manager funds it tracks, points the other way for the smallest and most specialized vehicles.

In the first half of 2026, close to 90% of the limited-partner commitments that closed went to funds below $15 million, and roughly 70% went to seed-stage funds, the ones writing the first institutional checks into brand-new startups[10]. And it took 64 days when the managers considers the process as a sales process with fixed sales pipeline, building a targeted list of the right LPs and following up instead of relying on warm introductions.

Capital is hard to raise for an emerging manager. In Q1 2026, family office, a private office that manages one wealthy family's money is a better bet than institutional investor.

The two-tier venture market, Q1 2026

| Layer | Who wins | Who struggles |

|---|---|---|

| Companies | AI platforms; late-stage AI priced ~3x non-AI[11] | Non-AI startups; angel activity slowed |

| Geography | United States, 83% of global dollars[1] | Most regions outside the US and China |

| Funds (GPs) | Top five firms, 73.1% of LP capital[7] | Mid-size generalist Fund I and Fund II managers[9] |

| Small / specialized funds | Sub-$15M seed funds with a clear sector edge[10] | Undifferentiated $50M to $250M generalists[8] |

Fund Concentration by country: United States, China, and Europe

United States companies raised $247 billion, or 83% of global venture capital, up from 71% a year earlier, which means the United States won most funds while all other countries shrank in relative terms[1].

More money into AI and far fewer companies funded overall is the same trend seen globally.

After the United States, China followed at $16.1 billion and the United Kingdom at $7.4 billion, each a small fraction of the American total[1]. The size gap is expected. What is more interesting is that the two countries reached their numbers in opposite ways. China is the world's second-largest venture market, and it is held there by a constraint - export controls cut it off from the most advanced AI chips [1].

Why, then, did its money flow into semiconductors, deeptech, and space rather than frontier models? Because China is funding the things it has been denied, building its own chip and hard-tech base to work around the cutoff. The United Kingdom is the reverse case. Its $7.4 billion leaned heavily on a single large autonomous-driving round and London's established fintech sector, a couple of standout deals outside a deep AI ecosystem[1][64].

European startups are now more aligned with the American market, raising $17.6 billion for the quarter, up nearly 30% from a year earlier, which on its own looks like good news. But two other numbers explain what is really going on. AI took more than half of all European funding for the first time, and the number of companies that got funded fell 40% from a year earlier[5]. This is EU’s determination to escape the America AI ecosystem. It meant there were a few casualties. Almost all of it was at the early end, with seed-stage deals down 44% and early-stage deals down 30%, while late-stage funding held steady[5]. The companies that disappeared were mostly young ones raising their first or second round, and the sectors that lost the most were the ones that could not claim any AI story.

Climate and clean tech fell the furthest, traditional software companies began struggling to raise their next round as investors asked why they were not built on AI, and conventional fintech and biotech without an AI angle were passed over[62]. The money in Europe moved up the ladder into a few large, late AI rounds and away from the broad base of ordinary early-stage companies.

Implication for the VC professional

Target The top 5 VC Firms

As a junior trying to break in, yes, they're worth targeting, but understand that you're joining a capital-allocation machine, not a classic startup. The work at a16z or Thrive is increasingly access, structuring, and managing billion-dollar positions, not finding unknown founders. If that's the job you want, target them. If you want to actually pick early companies, the five are the wrong room, and the small specialized funds are where that work still happens.

If you are an emerging manager (Fund I-III)?

Go small and narrow, not broad.

Sub-$15 million, seed-stage, single-sector funds are still raising; undifferentiated $50-250 million generalists are not.

Pick one sector where you have a real edge (defense, robotics, manufacturing, vertical software the AI rush ignored), and raise from family offices, which decide faster than institutions. Treat fundraising as a sales pipeline with a targeted LP list and follow-up, which can close in ~60 days.

If you are a mid-size generalist?

This is the most challenging position to be in Q1 2026 - too big to be specialized, too small to access the AI mega-rounds.

The strategy is to pick a side.

Either shrink and specialize into a defensible niche, or build a genuine edge in the non-AI sectors with less competition (real unit economics, profitability, moats against AI disruption).

For aspiring VC and MBA applicants

The skills that matter for VC applicants are observation, deep analysis and networking.

Observation: The record $297 billion looked like a broad trend, yet the median Series A was half the average and fewer companies got funded. Such breaking down data to its fundamentals is expected. What makes a VC candidate useful is their awareness of fund deployment by stage, sector, and geography, like the way Europe's 30% rise in deal value mostly in AI even though the total deal volume dropped by 40%.

Analysis: A VC must think in systems and second-order effects. The concentration of funds into five firms should be first analysis. A DPI of 0.27x as a cautionary tale for future fund allocation must be the second-order thinking.

Networking: Without talking to experts across functions and industries, the analysis will be superficial. The next fund could be deployed by a family office. Knowing them beats a warm introduction to a company that is already oversubscribed.

Venture Capital Industry Trend Q1 2026 #3: Stress Test for the AI Boom with SpaceX IPO

Take those five out and the total drops by 86.6%[2].

The stress test is happening now: SpaceX is the live test for OpenAI and Anthropic

By the time this report is published, the test had moved from hypothetical to live.

SpaceX filed its S-1 on May 20, 2026, opened its roadshow on June 4, and is set to price on June 11 and trade on June 12 on Nasdaq under the ticker SPCX, targeting about $135 a share for a raise near $75 billion at roughly a $1.75 trillion valuation, which would be the largest IPO in history[40].

The reason how SpaceX stocks perform matter for the entire AI industry and the VC community is that it is the first time public markets are asked to price one of the named brands against the private market at a scale similar to AI firm’s valuation.

SpaceX's most recent secondary cleared around an $800 billion valuation. The listing asks the public to roughly double the last private fundraising.

At $1.75 trillion, the company would trade near 94 times its 2025 revenue while carrying about $4.94 billion in GAAP losses and absorbing an xAI unit that burned $2.5 billion in Q1 2026 alone[40].

What is the pass condition?

The pass condition is if SpaceX prices are at or above its $135 target, opens above it on June 12, and holds the roughly $1.75 trillion valuation through the first weeks of trading, which means the public market is willing to pay about 94 times the company's 2025 revenue and look past $4.94 billion in losses and xAI's $2.5 billion quarterly burn[40].

The real test comes about six months later, at the December 2026 lockup expiry, when early employees, early investors, and the bank syndicate are first allowed to sell at once.

If the stock absorbs that wave of new supply and stays above $135, the public market will have ratified a price nearly double SpaceX's last private valuation of around $800 billion, and the signal to every private investor is that public investors will pay up for these names[40].

What is the failure condition?

The failure condition is any outcome that prices these companies below their private valuation.

It takes three forms, in rising order of damage.

First, a weak debut - SpaceX prices below the $135 range or breaks issue price on June 12 (Very unlikely as the stock is 4x oversubscribed)

Second, a fade out. The stock holds early on trading volume but drifts back toward the ~$800 billion private valuation as more shares are traded over the next few weeks.

Third, the stock sells off through the December 2026 expiry when insiders can finally exit, revealing that demand only ever existed for the small number of shares trading at first.

Any of the three tells every holder of a large private stake that the public market will not pay what the private valuation assumes[40].

OpenAI and Anthropic will then face extra pressure to delay or to list lower.

It could pop the entire AI bubble if Anthropic’s valuation doesn’t meet the market expectations.

Notable venture exits, Q1 2026

| Layer | Who wins | Who struggles |

|---|---|---|

| Companies | AI platforms; late-stage AI priced ~3x non-AI[11] | Non-AI startups; angel activity slowed |

| Geography | United States, 83% of global dollars[1] | Most regions outside the US and China |

| Funds (GPs) | Top five firms, 73.1% of LP capital[7] | Mid-size generalist Fund I and Fund II managers[9] |

| Small / specialized funds | Sub-$15M seed funds with a clear sector edge[[10] | Undifferentiated $50M to $250M generalists[8] |

Implication for the VC professional

Treat the SpaceX listing as a live readout and manage to it.

Watch whether it holds $135 and the $1.75 trillion valuation through the first weeks and survives the December 2026 lockup.

If it clears, the IPO path has reopened.

If it breaks, prioritize sponsor-to-sponsor sales, strategic M&A, continuation vehicles, and foreign listings.

For aspiring VC and MBA applicants

Observe where Space and defense tech are moving. They are backed by real government demand and 16z's American Dynamism thesis.

If you want an edge, build real fluency in one of these hard-tech sectors (defense, space, robotics, manufacturing) that software generalists cannot fake.

Just know the tradeoff. Investing in hard-tech sectors require patient capital in a regulated, slow to exit, market that rewards people who understand the business.

Venture Capital Industry Trend Q1 2026 #4:Venture Moved Into the Physical World

Beyond the three frontier labs, ten more companies raised rounds of $1 billion or more in sectors that included physical AI, autonomous vehicles, semiconductors, data centers, robotics, defense, and prediction markets[1].

What "Physical AI" is, and why Waymo raised $16 billion

Physical AI is the application of models to machines that act in the real world, including self-driving vehicles, robots, and the infrastructure that powers them.

Waymo's $16 billion round placed a self-driving company among the four largest venture rounds of the quarter, alongside the frontier labs, which shows the pivot in investor’s mindset where fleet hardware, sensors, and operations are treated as a venture-scale category instead of a research project[1].

The seed data points towards the same direction.

Crunchbase found that a majority of the largest recent seed rounds went to companies at the intersection of AI and the physical world. The shift is across all stages of startups[6].

Is infrastructure a real bet?

For two decades, venture optimized for one cost dynamic.

Software with 80%+ gross margins, where each new customer cost almost nothing to serve and growth requires little capital.

A self-driving fleet or a robot has factories, sensors, vehicles, depots, and people carries low gross margins, heavy capital needs, and a cost that rises with every unit deployed.

The reason the money is moving into the new cost dynamic is that the physical burden of building an ecosystem where people, machine and AI co-exist as equals is the new moat.

A pure-software AI wrapper can be copied in a quarter. A licensed, road-tested autonomous fleet with manufacturing and regulatory approval cannot be mimicked without effort and collective intelligence.

Frontier-lab and infrastructure growth assumes the power and data-center capacity to run the models will exist, and that assumption is under strain as grid connections and construction timelines lag demand[3]

The access to energy through grid, from plan to market takes more than four years, and global data-center capital spending is forecast at about $2.9 trillion through 2028, a figure too large for corporate balance sheets and bank lending to carry alone.

The overbuild risk is real just like the Fibre Optics craze of 1997. An investor backing a company that depends on AI compute now has to do due diligence and check whether the power contracts, the grid connection, and the build schedule are real before the financial model are even validated.

The deeper shift is who funds the buildout, because it is moving from equity to debt. Ropes & Gray estimates an $800 billion opportunity for private credit in AI infrastructure through 2028, with private credit already supplying about 60% of early-stage AI infrastructure development capital and moving from a supplemental source to a core financing mechanism[56]

A venture-style equity loss is capped at the investment, but a debt-financed buildout adds leverage and fixed obligations to the AI economy.

A demand shortfall would hit lenders and the cost of capital, not just the equity holders, which is the same systemic interdependence the circular-financing in earlier quarters produced, but the scale now is much larger and systemic.

Physical-world venture categories drawing $1B+ rounds, Q1 2026

| Category | What is being funded | The diligence question |

|---|---|---|

| Autonomous vehicles | Fleets, sensors, operations (Waymo $16B)[1] | Unit economics per vehicle-mile and path to scale |

| Robotics / physical AI | Hardware plus model integration[1] | Capital intensity against a software-style growth curve |

| Data centers / infrastructure | Compute capacity and siting[1][3] | Are power contracts, grid access, and build schedule real |

| Semiconductors | Custom accelerators and supply[1] | Foundry access and design-to-deployment timeline |

| Defense, energy, prediction markets | Dual-use and frontier categories[1] | Regulatory exposure and procurement timelines |

Implication for the VC professional

Underwriting in VC asks for a skill software ventures never had.

A VC professional must learn to do due diligence around the physical buildout before the financial model is evaluated.

They should confirm the power contracts, the grid connection, and check if the build schedule are real before trusting the deck.

The average grid wait time in primary markets now exceeds four years.

A financing plan should be based on these physical constraints.

With private credit already supplying about 60% of early-stage AI infrastructure capital, a demand shortfall will affect the cost of capital across the VC ecosystem[56].

For aspiring VC and MBA applicants

Stop reaching for the SaaS playbook on every deal.

You should be able to lay out why a robotics or data-center company carries utility-style costs under software-style growth, and what a power-purchase agreement or an interconnection queue does to a model.

An applicant should study the histories software people skip, from the fiber-optic glut, to railroads to utilities, because physical AI will have similar cycles like the infrastructure build-outs of the previous centuries.

Network with operators who run data centers, fleets, and energy contracts, because they see the constraints a model hides.

What to watch in Q2 2026

• Private valuation versus public multiples: whether a frontier-lab filing will test the downside protection, and if the lower ends are tested in public filing will it affect private valuation of the entire AI industry [7][12]

• The IPO reopening: whether software multiples recover enough for a late private round to list at or above its last private valuation, and whether the backlog forces the IPO to open in late 2026[1]

• DPI and LP behavior: whether distributions improve enough for endowments to recommit beyond the top five firms, or whether the concentration deepens to these firms, which are AI and Dual-Tech focussed [14][8]

• The non-AI seed market: whether seed deal counts stabilize or keep falling as the dollar total stays inflated by larger AI rounds[1]

• Physical-AI economics: whether power, grid access, and build timelines let the autonomous-vehicle, robotics, and data-center rounds to convert capital into deployment[3]

References

- Gené Teare, Q1 2026 Shatters Venture Funding Records As AI Boom Pushes Startup Investment To Nearly $300B, Crunchbase News, April 1, 2026 (data as of March 31, 2026) ↩ ↩ ↩ ↩ ↩ ↩ ↩ ↩ ↩ ↩ ↩ ↩ ↩ ↩ ↩ ↩ ↩ ↩ ↩ ↩ ↩ ↩ ↩ ↩ ↩ ↩ ↩ ↩

- Q1 2026 PitchBook-NVCA Venture Monitor, PitchBook and the National Venture Capital Association, April 2026 (deal value $267.2B and exit value $347.3B, each falling 73.2% and 86.6% without the top five; top five deals $195.6B; 73.1% of new commitments to five firms; aggregate unicorn value $5.8T with 44.6% first funded in 2016 or earlier; median DPI below 1x and single-digit IRR for recent vintages; median seed pre-money $18.4M; 88.8% of deal value and 42.5% of deal count in AI; more $1B+ funds closed in Q1 than in all of 2025) ↩ ↩ ↩ ↩ ↩ ↩ ↩

- Q1 2026 AI VC Trends, PitchBook, Q1 2026 ↩ ↩ ↩ ↩ ↩

- Q1 2026 PitchBook Analyst Note: VC Investment in Consumer AI, PitchBook, March 18, 2026

- AI Drives Europe's Second Straight Quarter Of Funding Gain As Deal Volume Falls Sharply, Crunchbase News, April 14, 2026 ↩ ↩

- The Largest Recent Seed Rounds Are All For AI Companies, Crunchbase News, March 31, 2026 ↩

- VC Funding Q1 2026: Record $330.9B and 80% AI (KPMG Venture Pulse and CB Insights totals; LP concentration; Anthropic valuation move; SpaceX/OpenAI/Anthropic value estimate), Angel Investors Network cross-source analysis, 2026 ↩ ↩ ↩ ↩ ↩ ↩ ↩ ↩ ↩

- What's Ahead For Startups And VCs In 2026? Investors Weigh In, TechCrunch, December 26, 2025 (DPI drought, endowments in repair mode, family offices) ↩ ↩ ↩ ↩

- Brett Calhoun, Raising a VC Fund in 2026, Redbud VC via Medium, March 24, 2026 (emerging managers 23% of fund value in 2024) ↩ ↩ ↩

- Record-Breaking Momentum in Emerging VC, VC Lab / govclab, June 1, 2026 (~90% of H1 2026 commitments to sub-$15M funds; ~70% seed-stage; ~64-day first close) ↩ ↩ ↩

- AI Boom Masks Fundraising Struggles For Non-AI Startups, TechCrunch (two-tier market; AI late-stage priced ~3x non-AI per Redpoint/SaaStr) ↩ ↩ ↩ ↩

- Crystal Ball: Will the AI Bubble Burst or Balloon in 2026?, Fortune, January 5, 2026 (practitioner views: Case, Clark, Kim, Okike, Das) ↩ ↩ ↩ ↩ ↩ ↩ ↩ ↩ ↩ ↩

- Benchmark's Bill Gurley: The AI Bubble Is About To Burst, And A Reset Is Coming, Fortune, March 17, 2026 ↩ ↩ ↩

- Capital Concentration: The Two-Tier Venture Capital Market, Esinli Capital, April 14, 2026 (median DPI 0.27x for 2017 vintage; A-to-B graduation rate) ↩ ↩ ↩ ↩

- EWVC January: Understanding U.S. Endowments, European VC Fundraising 2026 (Harvard ~$1B and Yale ~$6B secondary fund-stake sales; LP Perspectives 2026), European Women VC, January 27, 2026 ↩

- Chamath Palihapitiya, Deep Dive: Where Value Accrues in the AI Stack (six layers: infrastructure, chips, data, models, execution, application; fulcrum assets and chokepoints), May 1, 2026 ↩

- AI Infrastructure: The New Industrial Stack, Battery Ventures, March 19, 2026 (infrastructure favored over application; cost curves beat feature cycles; xAI Colossus ~$10B) ↩

- AI Infrastructure Roadmap: Five Frontiers for 2026, Bessemer Venture Partners (memory and context layer, evaluation and observability as emerging infrastructure as models commoditize)

- The Five Layers of AI: Where Are the Investing Opportunities Across the AI Stack (Jensen Huang's March 2026 five-layer cake: electricity, chips, data centers, models, applications), Hargreaves Lansdown, April 22, 2026

- AI Funding in 2026: Where Venture Capital Is Going, The AI Insider, May 27, 2026 (application layer more grounded than headlines; macro versus micro)

- AI-Focused VC Firms and Investors by Stage and Founder Fit (2026), Sky9 Capital, May 8, 2026 (AI = 53% of global VC in H1 2026; defensibility via proprietary data, novel architectures, deep workflow integration versus thin wrappers; source vcsheet.com)

- Q1 2026 AI Funding: 80% of VC Capital Went to 4 Companies, Angel Investors Network, 2026 (non-AI ~$60B across ~326 deals; most non-AI rounds sub-$10M; defense revenue visibility; angel and patient-capital opportunity)

- Q1 2026 Venture Capital Hits $297B: AI Captures 81% of Record Funding, Tech-Insider, April 19, 2026 (non-AI ~$57B; inflation-adjusted below Q1 2020; SaaS under pressure as agents automate workflows)

- Crunchbase Predicts: Why Top VCs Expect More Venture Dollars, Bigger Rounds And Fewer Winners In 2026, Crunchbase News, December 23, 2025 (climate and crypto lose share; vertical SaaS without an AI moat hard to fund; defense and healthcare-AI gain)

- 5 Startup Sectors Seeing Big Funding Growth, Crunchbase News, February 18, 2026 (fintech $53.8B 2025; Polymarket, Kalshi, Binance; robotics ~$14B; cybersecurity up but below 2021 peak; defense leaders)

- Fintech Startups Globally Raise More Money In Far Fewer Deals In Q1 2026, Crunchbase News, April 10, 2026 (fintech $12B / 751 deals, +5% dollars and -31.5% deals YoY, -33% QoQ; US $6.3B, +47% YoY; 2025 total $53.8B, +29.3%)

- Sector Snapshot: Defense Startup Funding Hits An All-Time Record As VCs Begin To Eye Exits, Crunchbase News, June 2026 (defense category over $14.6B in 2026 YTD past $9.6B record; Anduril $5B at $30.5B; 107 rounds; True Anomaly, Sierra Space, Vast; Swarmer IPO)

- Defense Tech Startups Had Their Best Funding Year Ever In 2025, Defense News, January 20, 2026 (defense-tech VC exits $54.4B in 2025 from $18.2B in 2024; active defense investors up 41%; Helsing €12B)

- Series A Metrics VCs Expect in 2026, CRV, March 31, 2026 (compute economics, usage depth, workflow entrenchment, path to software-like gross margins; revenue per employee as the efficiency signal)

- ValuStrat, Beyond the Hype: The Strategic Financial Metrics That Define AI Startup Valuation in 2026, February 3, 2026 (burn multiple adjusted for subsidized inference; price the trajectory not the margin; AI story versus AI asset)

- Startup Traction Metrics That Matter to VCs in 2026, Unicorn Screener, 2026 (burn multiple, David Sacks reading of 1.5x and 5x; gross margin as business-model verdict; NRR median 106%; CAC payback 18-month hard stop)

- VCs Now Demand Series A Metrics at Seed Stage, Pitchcasck, February 12, 2026 (Series A bar $2 to $3.5M ARR; burn multiple under 1.5x; NDR 110%+; revenue per employee over $200K)

- AI Startup Metrics: What VCs Want to See, Phoenix Strategy Group, 2026 (ARR per FTE $200K+; burn multiple under 2x; AI-specific indicators: model accuracy, inference cost, data-acquisition cost trend)

- VC Metrics for Robotics and AI Startups, Scaling Deep Tech, November 12, 2025 (robotics 30 to 50% gross margins; burn multiple 1.5x to 3x; AI-powered diligence improves red-flag identification ~40%, evaluates 5 to 10x more data points)

- Data Centres & AI Compute Infrastructure Insights 2026, Clifford Chance (underwrite to contracted revenue and take-or-pay; guaranteed capacity and performance metrics; GPU 3 to 5 year economic life; financeable offtake and new diligence items)

- The Neocloud Is Not Overflow. It Is the Third Pillar of AI Infrastructure, Global Data Center Hub, April 17, 2026 (CoreWeave $66.8B backlog; debt repayment depends on utilization above 80%; GPUs amortized over six years but obsolete in three to four)

- Neocloud Infrastructure, MLQ.ai, November 30, 2025 (combined contracted backlog near $100B; risk profile closer to infrastructure than software; customer-concentration and leverage/refinancing risk)

- Anthropic Closes $30 Billion Funding Round, CNBC, February 12, 2026, and Anthropic Finalizes $30 Billion Funding at $380 Billion Value, Bloomberg (round led by GIC and Coatue; D.E. Shaw, Dragoneer, Founders Fund, ICONIQ, MGX co-leads; Microsoft, Nvidia, BlackRock, Fidelity, Sequoia, plus Qatar Investment Authority, Temasek, and memory makers Micron, Samsung, SK Hynix in the later round)

- OpenAI's $122B Raise at $852B Valuation, Tech-Insider, June 2026 (Amazon $50B lead, Nvidia $30B, SoftBank $30B, Andreessen Horowitz co-lead, MGX, BlackRock, Fidelity, T. Rowe Price; Amazon up to $33B and Google up to $43B committed to Anthropic; OpenAI IPO prep, S-1 window Q4 2026)

- SpaceX IPO, Capital.com (drawing on Reuters and Bloomberg, June 2026): S-1 filed May 20, roadshow June 4, pricing June 11, Nasdaq debut June 12 under SPCX; ~$135/share, ~$75B raise, ~$1.75T valuation (~94x 2025 revenue), ~$4.94B GAAP losses, xAI ~$2.5B Q1 2026 burn, ~$800B prior secondary, December 2026 lockup ↩ ↩ ↩ ↩ ↩

- Vertical AI Is Eating Horizontal SaaS, BuildMVPfast, March 8, 2026 (Harvey $195M ARR, +290%, legal docs across 59 countries; Abridge $117M contracted ARR, 1.5M encounters, Epic distribution; EvenUp; NFX survey: more than half of VCs name proprietary data as the durable moat)

- The AI Startup Playbook: What's Actually Working in 2026, Featherflow, May 4, 2026 (Cursor $2B revenue in ~30 months; Harvey used by half of top US law firms; Lovable $100M with 45 employees; ElevenLabs $300M+)

- AI Agent Revenue Leaders, CB Insights, 2026 (coding AI agents most capital-efficient at ~$1.4M revenue per employee versus ~$594K across top agent categories; customer-service agents at 219x revenue multiples)

- The Intelligence Race: 3 AI Company Types Defining the 2026 Market, The Branx, March 27, 2026 (top early-stage AI firms over $2.5M revenue per employee with teams under 50; product-market fit 2.4x faster than traditional SaaS)

- State of Pre-Seed: Q1 2026, Carta (the disappearing middle, $1-2.5M rounds fell from 24% to 18% of pre-seed deals 2023 to 2026; AI rose from ~30% to 50% of pre-seed dollars; convertible notes a record-low 7% of rounds; the South overtook the Northeast in US share)

- The Real State of Seed Today: Top 10 Learnings from Carta's Latest Data, SaaStr, December 11, 2025, with CB Insights Q2 2025 and Carta State of Private Markets (AI = 42% of seed capital, up from 23% pre-ChatGPT; AI seed median $4.6M, ~1.3x the market; 95th-percentile seed valuation $80.5M; seed-to-A step-up 2.6x; AI valuation premium 38% at Series A and 193% at Series E+)

- State of Pre-Seed: 2025 in Review, Carta (US startups raised $10.4B across 50,316 financings in 2025, roughly flat on 2024 in dollars but down 13% in count; post-money SAFE cap is the standard instrument; median caps $10M for sub-$1M rounds and $15M for $1-2.5M rounds)

- Seed Round Valuations 2026, Flowjam (median seed pre-money ~$16M, up 19% even as seed activity fell 29% YoY; sector medians: AI/ML infrastructure $4.6M, healthcare/biotech $4.6M, fintech $3.2M, SaaS $2.8M, consumer $2.1M; 70+ AI-agent startups in YC's Spring 2025 batch)

- Seed-Stage SaaS Valuation 2026, SaaSValuationMultiple (SaaS seed median $19.8M post-money; AI-SaaS seeds ~$19M versus ~$15M for non-AI; 95th-percentile round $16.6M, more than 4x the median; median dilution ~19-20%)

- The State of Seed and Pre-Seed in 2025, VC Cafe, December 12, 2025 (Thinking Machines Lab's record $2B seed at a $12B valuation; broader-market median seed raise ~$3.6M; dilution stuck near 20%; 92% of pre-seed rounds on post-money SAFEs)

- Series A Funding Slides in Q2 2025, Carta, September 2025 (median seed-to-Series A interval reached 616 days, about twenty months; Series A cash raised down 23% to $4.7B; median Series A pre-money valuation an all-time high near $49.3M)

- A Guide to the Circular Deals Underpinning the AI Boom, Bloomberg, March 11, 2026 (Microsoft, OpenAI, Nvidia, and Amazon investing in one another while buying each other's products; interlinked commitments above $800B raise the risk of cascading losses)

- Noah Smith, Should We Worry About AI's Circular Deals?, Noahpinion, October 2025 (the distinction between vendor financing and round-tripping; the two fears of inflated revenue and tightly bound systemic risk; OpenAI losses reported tripling toward $14B in 2026)

- Nvidia Deals: Round Tripping or Vendor Financing?, Real Investment Advice, February 12, 2026 (telecom-era parallels: Lucent and Nortel lending customers money to buy their equipment, Global Crossing and Qwest trading capacity to book revenue, and the cascading failures that followed)

- Nvidia-OpenAI Deal Sparks Concerns Over Circular Financing in AI Boom, Business Standard citing Bloomberg and Bernstein Research, September 2025 (Bernstein's Stacy Rasgon on the circular concern; Nvidia in more than 50 AI venture deals per PitchBook; Jensen Huang in March 2026 calling the $30B OpenAI stake possibly its last; European competition staff reviewing the spending)

- Artificial Intelligence Q1 2026 Global Report, Ropes & Gray, May 2026 (drawing on PitchBook, Morgan Stanley, Blackstone, Deloitte, NVIDIA: Q1 M&A value up 2,486% YoY and VC value up 613% YoY; 79% of global VC funding to AI; data-center CapEx forecast at $2.9T through 2028 with an ~$800B private-credit opportunity and private credit supplying ~60% of early-stage AI infrastructure capital; average grid-connection waits past four years; only 21% of leaders hold a mature governance model for autonomous agents; frontier models from Google, OpenAI, and Anthropic tied on the Artificial Analysis index with cost-efficiency now the battleground; hyperscaler CapEx at about 25% of revenue versus 408% in the dot-com build and 189% in the 1869-1888 railroad build) ↩ ↩ ↩ ↩

- Pershing Square Holdings Annual Investor Presentation, February 11, 2026 (Alphabet top contributor at +10.3% gross, described as one of the clearest beneficiaries of AI integration; Amazon added as the largest cloud business by market share; PSH NAV up 20.9% in 2025 but down 5.4% year to date by February 9, 2026 amid the early-year selloff)

- China property problem: Bigger than Mt. Evergrande, Putnam Investments (Chinese real estate a roughly $50 trillion asset class, about 2.5 times the US market in 2007; about 70% of urban household wealth in housing; real estate directly and indirectly near 29% of GDP; notably fewer derivatives and collateralized debt obligations than the US 2008 episode; Evergrande with 1.5 million buyers awaiting unfinished homes) ↩ ↩

- Kenneth Rogoff, China's Real Estate Challenge, IMF Finance & Development, December 2024 (real estate and related sectors at roughly 25% to 30% of China's GDP, exceeding the US's about 18% and the pre-2008 peaks of Spain and Ireland; the downturn concentrated in tier-3 cities that make up about 60% of GDP, echoing how US subprime concentrated in a few states before spreading) ↩

- China is Experiencing its Own 2008 Scenario, reporting Barclays estimates, May 2025 (the post-2021 property crash erased an estimated $18 trillion of household wealth, exceeding the inflation-adjusted $17 trillion lost in the US in 2008; property reached 25% to 30% of GDP and 70% to 80% of household wealth; Evergrande reported about $340 billion of liabilities; the high-yield property index fell more than 80% and home sales more than 50% in three years) ↩

- SCOOP: Thrive Netted 2.4x DPI from 2016 Fund. Here's Thrive's $10 Billion Pitch, Newcomer, February 2026 ↩

- AI Drives Europe's Second Straight Quarter Of Funding Gain As Deal Volume Falls Sharply, Crunchbase News, April 14, 2026 ↩