In Q1 2026, the General Services Administration forced $20+ billion in concessions, which had a ripple effect on a pricing model clients had been pushing for a long time: outcome-based pricing. AI accelerated the adoption. The most interesting development in the quarter was OpenAI's DeployCo announcement, which placed McKinsey, Bain, and Capgemini inside a $14 billion lab-consulting joint venture, forcing the asset-light partnership model that defined consulting for 50 years to reprice itself around outcome-based contracts.

Tl;DR

- GSA forced the top federal consulting firms (including Deloitte, Accenture, Guidehouse, and Booz Allen) to surrender over $20B in concessions and adopt Performance-based fees

- Deloitte eliminated traditional analyst-to-manager titles effective June 1, 2026. McKinsey shifting partner pay toward equity.

- Agentic AI's production scale prioritized with AI governance after Lilli breach

- EY released the first formal SaaS-style outcome pricing playbook in February 2026.

- OpenAI launched DeployCo ($14B valuation) with McKinsey, Bain, and Capgemini as partners.

- Anthropic quickly followed with a $1.5B Blackstone/Goldman-led consortium

- Microsoft dominates enterprise AI orchestration layer . No other platform is within 13 points.

- EU AI Act deadline on August 2, 2026; penalties up to 7% of global turnover

- KPMG became the first Big 4 firm to achieve ISO/IEC 42001 certification

- IEEPA ruling triggers trade advisory surge. Deloitte and EY-Parthenon set to benefit

We cover these 7 trends

Contents

- Trend #1: Federal Contract Reset and the IEEPA Ruling

- Trend #2: Agentic AI Gains Momentum

- Trend #3: Deloitte Scraps Traditional Consulting Roles & Slowdown at Entry Level

- Trend #4: Outcome-Based Pricing Becomes the Procurement Default

- Trend #5: Frontier Labs and the Threat to the Big Three

- Trend #6: EU AI Act Drives Compliance Demand

- Trend #7: Trade Advisory Becomes a Strategic Core Practice

Overview

Q1 2026 was the first full quarter where the consulting industry faced three shocks simultaneously: the executive order Promoting Efficiency, Accountability, and Performance in Federal contracting [40], the EU AI Act enforcement, which is likely to put some guardrails on AI training, set to go live on August 2, 2026 [41], and the production-readiness for agentic AI.

The three developments were predicted for Q4 2025, but two developments accelerated much before the 2027 timeline.

First, outcome-based pricing is the new norm in Federal contracts.

Contractors are now forced to offer discounts to retain contracts [1] The knock-on effect is that 73% of private-sector clients now favor value-based or outcome-driven pricing over hourly rates [2].

Second, the consulting roles were disrupted, with even large Fortune 500 companies aiming for a flat organizational structure.

Deloitte announced on January 22, 2026, that it would scrap traditional job titles across its US business effective June 1, 2026 [3], an acknowledgment that AI now handles the analyst-grade work the Consulting Pyramid structure was built to absorb.

Third, Clients were prioritizing large-scale transformations that include becoming AI-ready, with a slower pace and lower spend on smaller contracts. The margin-pressure faced by clients had a cascading effect on consulting projects, which were deprioritized or postponed, with the only exception in integrating AI into the workflow.

Trend #1: Federal Contract Reset and the IEEPA Ruling

GSA Crackdown Hardens Into a Permanent Pricing Reset

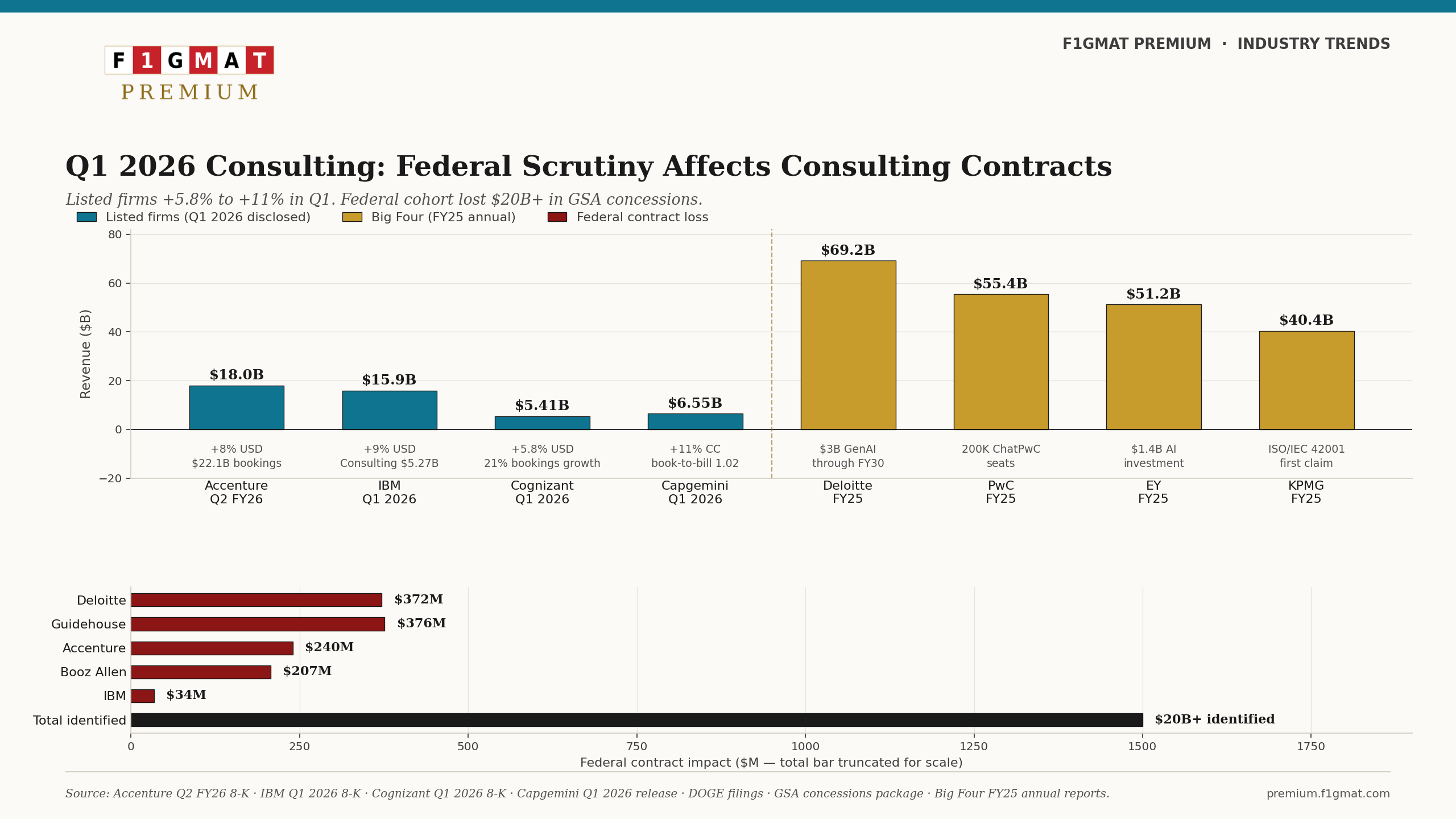

The General Services Administration named the ten highest-paid consulting firms (set to receive over $65 billion in fees in 2025 and future years) and ordered them to defend each contract or accept reductions [1]. By the deadline, seven of the ten had identified more than $20 billion in additional savings options [5] , offered through three levers: outright contract cancellation, price freezes, and a shift to performance-based fees.

The contract-level damage by Q1 2026 [6]

- Deloitte: 129 contracts have been terminated or downsized with approximately $372 million in revenue lost

- Accenture: 30 contracts cut, approximately $240.2 million claimed savings

- Booz Allen Hamilton: 61 contracts cut have been cut, with approximately $207.1 million in revenue lost

- Guidehouse (formerly PwC Public Sector): approximately $376 million in lost contracts

- IBM: 10 contracts cut, with approximately $34.3 million in claimed savings

The IEEPA Ruling: Feb 20, 2026

On February 20, 2026, the US Supreme Court issued its ruling on the International Emergency Economic Powers Act (IEEPA), the statute the administration has used to authorize broad tariff actions [7]. For consulting, this created a parallel pricing problem: clients running global trade exposure assessments suddenly needed scenario modeling for both the pre-ruling and post-ruling tariff stack, which has expanded the addressable trade advisory engagement.

The Pricing Mechanism Federal Buyers Want

In the concessions package, three of the ten named firms offered performance-based fees as a procurement option to retain contracts [1]. This is the first time outcome-based pricing has been formalized inside a federal consulting procurement. It is also why, as we will see in Trend #5, McKinsey is reportedly shifting more partner remuneration into equity to absorb the volatility that performance-based revenue introduces [8].

Implication for Consultants

Historically, Consultants at mid-career have been generating revenue on Federal Services accounts. The contract cancellation risks have disproportionally affected program management and even the implementation teams.

The move to performance-based fees changes the internal billability conversation.

For senior consultants, not used to the KPI pressure, lateral move within the firm to commercial-sector practices (where pricing pressure exists but is less acute) is one way to avoid the axe.

Another way to manage the change is by building credentials in trade advisory or sanctions compliance.

An even better way to manage the uncertainty is by moving to a regulated vertical like healthcare, financial services or energy where outcome-based pricing is the norm. With the team experienced in handling KPI, the struggle to adapt will be minimum.

For the Aspiring Consulting Applicant

- Build a vocabulary on outcome-based contracts covering retention triggers, KPI verification cycles, escrow structures and other jargons. The client conversation and vocabulary they use are now part of case interviews.

- Choose MBA electives where you have to apply your thinking within regulatory strategy, public-sector contracting, and outcome-based commercial models. Programs strongest here include Wharton (Public Policy and Strategy), Yale SOM (public-private partnerships), and Georgetown McDonough (federal contracting and network).

- Target firms with diversified federal-commercial mix. Pure federal specialists (Booz Allen, Guidehouse, CACI) carry concentration risk through the next 18 months that the diversified firms don’t face.

Trend #2: Agentic AI Gains Momentum

Agentic AI: Cloud Service Provider vs. Chip Manufacturer

In Q1 2026, 31% of enterprises had at least one AI agent running in production [9] and 80% of enterprise applications shipped or updated at least one AI agent, up from 33% in 2024.

The Average projected AI spending in the US over the next 12 months: $207 million per organization, nearly double the same-period figure a year ago, and more than the $186 million seen in the rest of the world.

The gap in AI spending when comparing US with the rest of the world is shortening, according to the KPMG survey. However, there is a nuance in the spending.

Rise of On-Premise LLM

For segments serving sensitive data (HIPAA), data leaving the premise might be risky as breaches have huge regulatory cost – upto 7% of total global turnover or fines up to €35 million, whichever is higher, enforced through the EU AI Act Penalties.

Even regulated industries like Finance, Healthcare, and government have on-premise requirements for data residency.

Despite the initial investments, Lenovo's 2026 TCO analysis shows on-premise AI servers achieving breakeven in under 4 months for high-utilization inference, with 8-18x lower cost per million tokens vs. cloud APIs or IaaS [42].

Cloud Service providers have responded with hybrid models like AWS Outposts, Azure Stack, or sovereign clouds to capture hybrid demand.

In AI’s need to keep the great AI reset story alive, the line between manufacturers, vendors, consulting companies, and cloud service providers is thinning as hardware vendors like NVIDIA, Dell, and Lenovo are gaining revenue through on-premise software stacks. From pure GPU play, these manufacturers are deploying bundled software or proprietary tools for easier deployment and management.

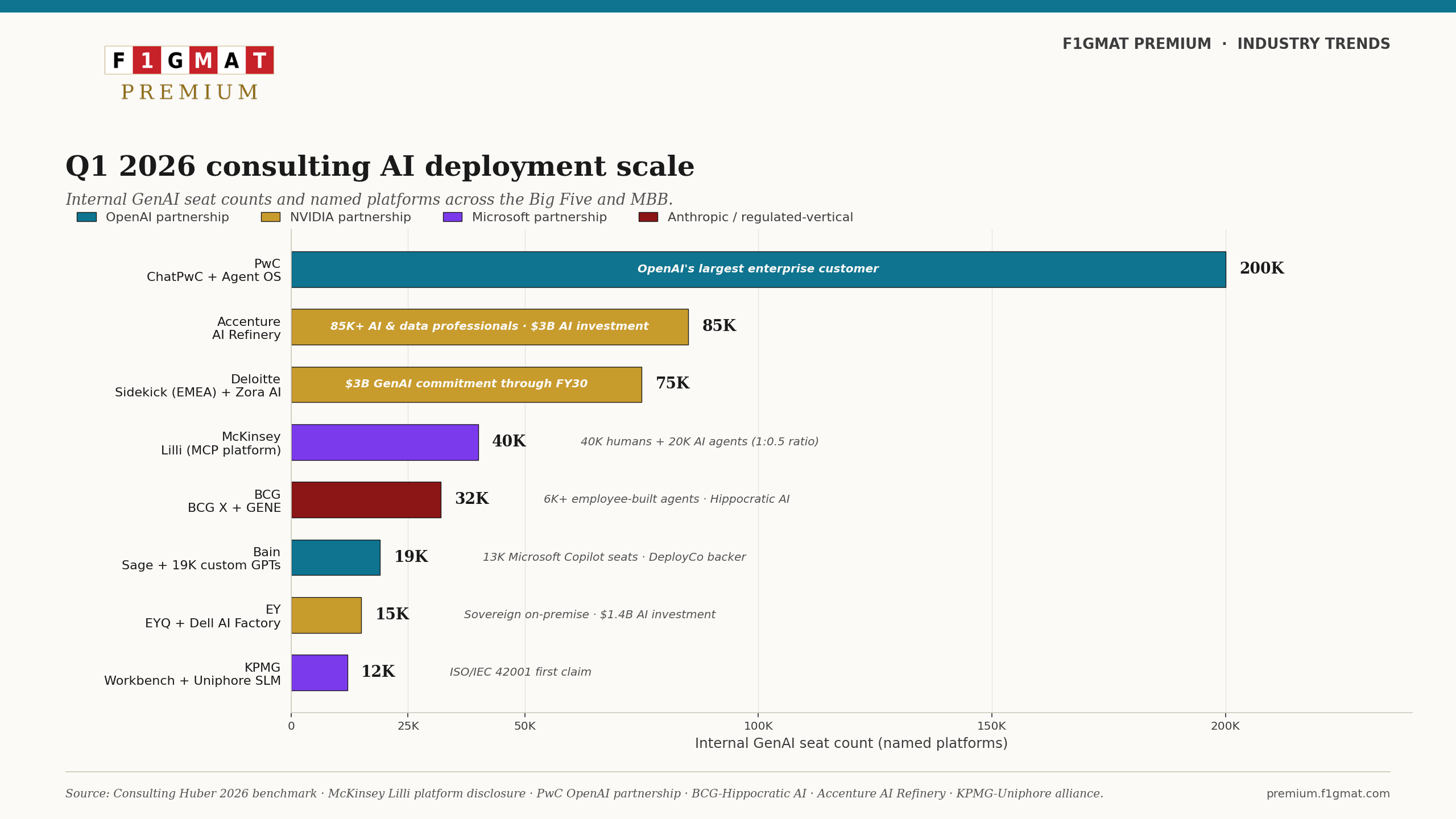

Firm-by-Firm Q1 2026 Agentic AI Deployment

The proprietary internal GenAI assistant (Lilli, Sage, GENE, EYQ, ChatPwC, Workbench, PairD) is no longer a productivity accelerator.

As per the April 2026 Consulting Huber benchmark, it is the cost of entry [22] determined by the governance posture and the knowledge of the regulated industry that limits firms in Q1 2026 from adopting Agentic AI at scale.

McKinsey: Lilli Becomes an Agentic Orchestrator and Gets Breached

A cautionary tale on redesigning existing knowledge or GenAI internal knowledge assistant to an Agentic AI came through Lilli, a multi-model agentic orchestrator running on the Model Context Protocol [32]

Started in 2023 as a chatbot with superpowers (it held user information in the same database), the bot was the first AI internal chatbot that powered the engagements for McKinsey's 40,000 consultants.

By March 2026, the firm reported a workforce mix of 40,000 humans plus approximately 20,000 AI agents (up from 3,000 in late 2024), with Lilli handling over 500,000 prompts per month and 70%+ active usage across the firm [39]

Then on March 9, 2026, CodeWall, a security company disclosed that by using their autonomous agent and a methodical, three-step process based on SQL injection on an unsecure JSON endpoint, they could gain read-write access to the production database within two hours. [33]

Over 46.5 million chat messages, 728,000 files, 57,000 user accounts, 3.68 million RAG document chunks, 384,000 AI assistants, and the system prompts governing Lilli's behavior across 40,000 consultants were exposed.

McKinsey patched within 24 hours, but for the consulting industry, the breach became the 2026 case study on why agent-driven governance is far from reality for ecosystems where AI agents are participating in at least a 1:2 ratio to humans.

BCG: Hippocratic AI Alliance and the GENE/Deckster Build-Out

On January 8, 2026, BCG announced a strategic collaboration with Hippocratic AI to deploy agentic AI across biopharma and medtech, using Hippocratic's Polaris Constellation architecture [34]. The architecture follows a constellation of LLM approaches where, instead of one large LLM handling every touch point, one large conversational agent leads as the primary touch point for users, with multiple specialists running in parallel to validate and refine deliverables. The specialists are trained on one narrow domain, like medication safety, clinical escalation, nutrition, and even hospital policy.

The partnership is the first major breakthrough in the in-house vs. partnership agentic AI debate in highly regulated domains where consulting companies cannot enter as subject-matter-experts and as service providers capable of offering in-house AI agents.

Hippocratic had raised $404 million from Andreessen Horowitz, General Catalyst, Kleiner Perkins, NVIDIA's NVentures, and Google's CapitalG, and partners with more than 50 health systems and payers.

Such market validation rarely offers non-clinical Agentic AI solutions alone. The fully autonomous diagnosing and prescribing function is outside the purview of Hippocratic AI now, which, like many disruptive AI, is deterred by the EU AI Act high-risk rules and the FDA’s SaMD.

The EU AI Act (entered into Aug 2024) uses a risk-based framework where healthcare AI Agents are classified as high-risk (Annex III) AI systems that need human oversight to avoid risks to the health and safety of the users.

Under the FDA’s SaMD (Software as a Medical Device (SaMD)) regulations, Agentic AI falls under non-device Clinical Decision Support (CDS). If they choose autonomous functions, they will be regulated as devices, and the agents must be open to detailed documentation on design, data, validation, human-AI interaction, and post-market surveillance.

Although the partnership between BCG and Hippocratic AI is the first step to automate non-clinical functions, the recent job posting to hire Head of Regulatory Affairs [43], the reversal of the integrated “retail-healthcare-pharmacy” model as seem with the Sycamore Partners take-private of Walgreens, and over 40% of Gen Z and millennials reported using virtual visits, and many choosing retail or urgent care clinics at rates far exceeding older generations, has compelled providers to shift capital toward technology-enabled virtual delivery.

AI Agents in healthcare with privacy guardrails is an ideal technology enabler to expand into clinical settings.

BCG reported 25% of its $14.4 billion 2025 revenue (approximately $3.6 billion) came from AI-related work, up from $2.7 billion in 2024 [21]

Despite over a quarter of new business from GenAI, only 20% of clients reported an increase in revenue [44]. Partnering with specialist AI providers with access to data and a strong regulatory reputation is the next step for Consulting companies to maintain momentum, as GenAI and productivity improvement and its impact on revenues will take more time to realize. The follow-up consulting engagements will dry up.

OpenAI Lab-Consulting Partnership Model: DeployCo

Bain is following a different strategy. Bain's Sage chatbot is empowered by 19,000+ custom GPTs built by Bain employees [22]. The collaboration runs through a dedicated Center of Excellence and includes co-designed industry solutions.

The embracement of OpenAI is a signal by Bain to earn the exclusive partnership with OpenAI.

With record fundraising, OpenAI is exploring the option to scale a lab-consulting partnership model, where Consulting companies like Bain could deploy OpenAI’s latest models at scale in enterprises.

Despite the exclusive partnering positioning, OpenAI is not risking betting all their chips on Bain.

In May 2026, Bain was named alongside McKinsey and Capgemini as a consulting partner in OpenAI's Deployment Company (DeployCo), where Bain & Co. is also a backer [36].

Accenture-NVIDIA partnership: Lab-consulting partnership at hardware level

Accenture is staying outside the model deployment market and finding a niche by exploring consulting in the on-premise and local LLM level. But the niche is not a small niche. Accenture employs approximately 77,000 AI professionals (the largest cohort across the Big Five), against a $3 billion AI investment commitment.

By partnering with NVIDIA directly through Accenture’s AI Refinery Platform, the consulting giant is offering a "refinery" to convert NVIDIA AI technologies (foundation models, NIM microservices, NeMo, Omniverse, AI Blueprints, etc.) and "refines" them into production-ready, enterprise-grade, industry-specific solutions.

With Accenture's AI Refinery, the only consulting-built reference architecture inside NVIDIA's formal Business Group structure [22], the consulting giant’s expertise in adding layers of orchestration, governance, knowledge integration, and no-code tools is aimed at clients, who can move from experimentation to scaled agentic AI in days/weeks.

The collaboration plans have expanded to 100+ industry-specific AI agents (telecom, financial services, insurance, manufacturing, healthcare, retail.) and physical AI solutions in manufacturing.

Deloitte: Zora AI, the Consulting Title Reform, and the EMEA Sidekick Rollout

Deloitte has decided to disband the traditional pyramid model prevalent in consulting ( analyst, consultant, senior consultant, manager) [3]

Effective from June 1, 2026, the structural shift will impact ~181,500 U.S. employees across all divisions where analyst, consultant, and managerial roles will be replaced by roles specific to the function like “Software Engineer III,” “Project Management Senior Consultant,” “Senior Consultant, Functional Transformation” along with a new senior leadership tier called “Leaders” alongside partners, principals, and managing directors.

Deloitte has already tackled the internal productivity goals with Sidekick, a proprietary GenAI tool that automates presentations, code generation, project planning, emails, summarization, and brainstorming before interfacing with Client-Facing Agentic AI, Zora AI [35]

Deloitte’s agentic AI platform offers a suite of specialized digital agents that perceive, reason, and act autonomously across enterprise functions with a primary focus in Finance (expense management, financial statement analysis, scenario modeling), procurement, supply chain, sales & marketing, HR/human capital, and customer service[37].

Even within the suite of agents, the functions are divided into operational and advisory, with operational tasks like transaction processing and workflows managed by “Perform” agents and “Advise” agents focusing on analysis, insights, and decision support.

PwC: Agent OS at 200,000 Seats and OpenAI's Largest Enterprise Customer

PwC runs ChatPwC at approximately 200,000 internal users, the largest seat-count enterprise GenAI deployment of any consulting firm [22]

As OpenAI's first enterprise reseller and its largest enterprise customer, PwC also has an edge with its Agent OS platform [38] , which is designed as a unified “operating system” or command center for building, integrating, governing, and scaling multi-agent workflows across vendors (OpenAI, Anthropic, Google, Microsoft, AWS Bedrock, etc.) and integrates with major enterprise systems (SAP, Salesforce, Oracle, Workday, etc.).

The early adoption of Agentic AI and its impact on graduate intake – down 6% year on year is visible inside the Q1 2026 talent profile, where PwC has pivoted away from looking into technical skills for entry level profile and into judgment, communication, and teamwork.

EY: EYQ, Sovereign AI, and Trade Advisory Lift from EY-Parthenon

EY runs EYQ (its internal LLM) and is the only Big Four firm with on-premises Dell AI Factory deployments running NVIDIA hardware, which positions the firm for sovereign and regulated-industry mandates where data residency disqualifies cloud-first competitors [22]

Unlike competing consulting companies, which are diversifying their service delivery, EY is targeting hard-to-serve clients in the regulated industries (financial services, healthcare, government, life sciences), where cloud-AI or even providers with predominantly cloud offerings are disregarded for on-premise providers. By partnering with Dell and NVIDIA, EY has become the go-to partner for clients with high compliance barriers.

To sweeten the deal, EY on February 17, 2026, published the SaaS GenAI outcome-based pricing playbook under ASC 606, which ensures revenue is recorded when value is delivered to the customer, not just when cash is received, or a contract is signed. This means the clients are required to pay only if the designed task is delivered without human intervention [18]

Another unique M&A that is finally giving EY a market advantage is the 25,000-person EY-Parthenon strategy-and-transactions practice, which is the largest strategy consulting practice of any Big Four firm by headcount [31]

Although the strategy practice is demoted in favor of implementation in current consulting pipeline, the Parthenon team has strong implementation experience. The only risk is when Agentic AI scales to replace ‘strategy’ only talent. Then, expect a huge layoff cycle in the practice.

KPMG: Workbench, the Uniphore Alliance, and the Q1 2026 AI Pulse Data Set

KPMG Workbench and the KPMG-Uniphore strategic relationship (announced late 2025) anchor the firm's small-language-model approach for regulated industries (oil and gas, healthcare, telecommunications, financial services) [27].

KPMG is trying to capture volume and also address cost constraints that arise with LLM integration at scale.

By integrating Uniphore’s Business AI Cloud, Small Language Models (SLM) could be positioned for mid-market companies that want agentic AI without the cost associated with frontier models.

The deployment cycle is shorter, favoring enterprises that want a proof of concept with SLM before scaling with LLM. The positioning also favors KPMG to differentiate from the Big Four peers.

KPMG became the first large consulting firm to gain the ISO/IEC 42001 certification [22] . The pivot in skillset from implementation to orchestration to governance would mean teams strong in governance can handle the expectations of clients in regulated industries and also face the EU AI Act that could cost clients as much as 7% of their global turnover.

On March 31, 2026, KPMG released its Q1 AI Quarterly Pulse, which reported: 54% of organizations actively deploying AI agents (up from 11% two years earlier), $207 million average projected AI spend over the next 12 months, 63% requiring human validation of AI outputs (up from 22% in Q1 2025) [10] .

The jump in human validation from 22 to 63% is a sign that AI has matured from pilot to production-ready phase, with more human eyes on the deliverable to ensure that Agents don’t cross the governance layers and act in a way that jeopardizes client reputation and end users.

Agentic AI – Most Strong in Sales Development

Across functions, the time it took to recover the investments on AI agents was 5.1 months in Q1 2026, as per BCG and Forrester telemetry compiled in March 2026[9] .

Even within diverse functions, SDR (sales development representative) agents recovered the initial investment within 3.4 months when they could source 19% of new leads with agents in Q1 2026. The human-in-loop was the lowest in this function at 8% compared to 61% in Legal, the highest for any function.

| Function | HITL Rate | Median Payback | Notes |

|---|---|---|---|

| Marketing & SDR / Outbound | 8% | 3.4 months | Lowest HITL — narrow scope, high autonomy |

| Software Engineering | 21% | 6.2 months | Coding agents |

| Data & Analytics | 26% | 5.8 months | |

| Supply Chain & Logistics | 29% | 7.6 months | |

| Customer Service & Support | 32% | 4.7 months | Common escalation for complex cases |

| Finance & Operations | 37% | 8.9 months | |

| HR & People Ops | 44% | 9.4 months | |

| Legal & Compliance | 61% | 11.2 months |

HITL - Human in the Loop

Regulated functions - Finance, Supply Chain, HR, and Legal had higher Human-in-the-loop (HITL), not from technological complexity, but penalties for violations are higher in these functions.

As expected, the payback cycles of Agentic AI investments were higher in these functions, with Legal and Compliance taking 11.2 months.

Most human consulting opportunities in the next 2 years would be in regulated functions & industries, and in governance frameworks that need strong validation every step of the way.

Microsoft is The Orchestration Layer Winner

VentureBeat's VB Pulse Orchestration Tracker for Q1 2026 named Microsoft the enterprise default, with no other platform within 13 percentage points in February [11] . Copilot Studio and Azure AI Studio sit inside an enterprise stack that many companies already leverage (Microsoft 365, Teams, Entra ID, Azure) with existing procurement relationships. OpenAI was second, moving from 23.2% in January to 25.7% in February. Anthropic was the newcomer at the orchestration layer.

Buyers' demand for greater control over agents rose from 17.9% to 22.9% in just one quarter. Earlier, model quality and the ease of use of tools were bigger purchasing factors. The 'quality' as a selection criterion fell from 35.7% to 25.7% once AI models overcame the baseline on hallucination and accuracy.

The Governance Re-Architecture With Audit Trail

The McKinsey Lilli breach brought back the importance of humans in the Agentic AI loop and edge cases where Agents can go rogue.

Q1 2026 saw Cloud Native Computing Foundation release a Windows-native agent runtime leveraging Hyper-V isolation, each agent running in a micro-VM with its own virtual TPM [12]

By logging every tool call, data access, and inter-agent communication, with no option to delete the audit trail, regulated industries worried about large-scale breaches have a temporary solution.

Key Takeaways – Agentic AI Consulting

- Databricks Data (Feb, 2026): Multi-agent systems jumped 327% in under four months

- VentureBeat tracker: 4,800 production agent deployments across the Fortune 500 in Q1 2026

- BCG Survey: 22% of production deployments now coordinate three or more agents (BCG)

- Stack Overflow Developer Survey 2026: 71% of professional developers report using an AI coding agent at least daily

- MIT Sloan productivity study: 14% increase in shipped features per engineer-quarter for teams that deployed coding agents in 2025

- BCG Survey: 63% of leaders now require human validation of AI agent outputs, up from 22% in Q1 2025

- Lilli breach exposure: 46.5M chat messages, 728K files, 57K user accounts, 384K AI assistants

- Internal GenAI seat counts: PwC ChatPwC ~200,000; Deloitte Sidekick (EMEA) 75,000; McKinsey Lilli 40,000+; Bain Microsoft Copilot 13,000

Implication for Consultants

The most visible impact for consultants is through platform fluency in at least one Tier-1 agent orchestration platform (Salesforce Agentforce, Microsoft Copilot Studio, Agent 365, or ServiceNow AI Agents).

With loyalty shifting rapidly in the AI world, exposure to LangGraph or CrewAI will address the risk of putting all eggs in one orchestration basket.

The second and tougher skill to develop in a short time is to build adversarial judgment.

Consultants who can identify what an agent got wrong, fast, under pressure, are promoted faster than peers who accept agent output uncritically or reject it reflexively.

The McKinsey AI-assisted case interview is now testing for this skill in lateral hires.

The balance of practical experience and soft skills in adversarial judgement need valid governance credentials like IAPP AIGP, ISACA Certified AI Auditor, or ISO/IEC 42001 internal auditor in the next 12 months.

Post-Lilli-breach, every client engagement requires a defensible governance posture, and credentialed consultants are billable on those projects from day one.

For the Aspiring Consulting Applicant

The traditional case interview is being supplemented (at MBB) and partially replaced (at Big Four and AI lab joint ventures) with live AI-augmented exercises.

Applicants who walk in fluent only in classical case-cracking will find themselves competing with a candidate pool that also brings AI orchestration fluency.

The easiest step aspiring consultants can do now is to build a multi-agent system as a personal project, document the deployment publicly, preferably on your YouTube Channels and website.

A portfolio outperforms generic case prep best practices.

The second practical tip is preparing for and against AI-augmented case interviewers, where you have to defend or deconstruct judgment on a position, agents, or AI-generated recommendations. This skepticism needs validating sources and a wide readership that cannot be built in the short term. Read widely.

The most practical tip if you are planning to augment your resume with an MBA is to choose MBA programs where AI is part of the core curriculum in some form. Even data science in the core curriculum or flexible core with the option to add data science and AI in the core is a win.

In 2026, not many top MBA programs are offering this feature.

The second best bet is to choose an MBA program with concentrations in AI, where leadership courses have been extensively redesigned with AI as the backbone.

If you are targeting an MBA to join your dream employer, dissect their investments in AI infrastructure.

Old branding based on strategic consulting has little value.

Prioritize PwC ChatPwC (200K seats), Deloitte Sidekick (75K), McKinsey Lilli (40K), and Bain Microsoft Copilot (13K). They have shown the depth of internal AI infrastructure that new hires will work alongside.

Firms with thin internal AI capability cannot train junior consultants at a faster pace. In an AI-first world, speed is everything.

On the recommended reading, read the BCG-Hippocratic AI collaboration announcement, the Anthropic-Deloitte Zora AI partnership, and the Genentech gRED Research Agent case study before interview season.

Trend #3: Deloitte Scraps Traditional Consulting Roles & Slowdown at Entry Level

Deloitte Scraps Traditional Job Titles

On January 22, 2026, Deloitte announced internally that it would eliminate traditional job titles across its US divisions effective June 1, 2026 [3] . The change is explicitly framed as a response to AI's reshaping of how junior consultants approach tasks. The pyramid model, which depended on a wide base of analysts handling research, modeling, and data analysis, no longer matches the work distribution inside an engagement.

Deloitte committed $3 billion in generative AI development through fiscal year 2030 and launched Zora AI (an agentic model powered by NVIDIA) to automate complex business processes.

When a firm of Deloitte's scale strips the analyst, consultant, senior consultant, manager, senior manager naming convention, the replacement model (which Deloitte will detail in the coming months) is consistent with what industry observers have speculated and confirmed: a thinner base of juniors, a solid middle of subject-matter experts, and senior advisors at the top [13]

UK Big Four Graduate Intake Cuts (2023 to 2024 Cycle)

Graduate job postings in accounting and consulting dropped 44% year-on-year by 2024 across the UK market [13]. Unlike the US, where M&A deals even in an economic slowdown blossomed in AI with Private Credit playing an active role in building momentum, the UK’s economic slowdown and lack of buffer in AI investments with stronger offshoring, pushed the demand down. With AI tools and workflows available for clients, they pushed back against fees charged by juniors, crashing the demand for this cohort.

- KPMG UK: reduced 2023 graduate class by 29% (from 1,399 hires to 942)

- Deloitte UK: cut graduate intake by approximately 18%

- EY UK: cut graduate intake by 11%

- PwC UK: cut graduate intake by 6%

The Princeton Signal

Bloomberg's April 15, 2026, Businessweek cover documented the demand-side flip even at Princeton.

Two Princeton seniors who had co-founded an undergraduate consulting club and done summer internships at top-tier firms graduated in spring 2026: one went to Wall Street, the other to the UK government [14]. The students captured the cohort sentiment: those entry-level roles are slowly becoming obsolete.

As per Q1 2026 reporting, the candidates getting offers in 2026 are stronger than the 2023 peak cohort, as firms have become more selective, favoring communication, judgement and leadership over technical fluency [15].

McKinsey's Operating Adjustment

Layoffs are a side-effect of efficiency ever since the horse and buggy were replaced by cars.

McKinsey started its internal shuffle by eliminating 200 technology and professional support staff in late 2025. The judgment skills and EQ to address clients' concerns gained the most billing, as AI has not evolved to understand emotional cues in a live meeting. The global managing partner Bob Sternfels hinted that more non-client role reductions are on the way in the next two years [16].

Unlike the advent of automobiles, the white-collar jobs disrupted are industry-specific. A consulting company where reporting is standardized doesn't need talent for reporting or content production. They were the easiest functions to automate, as prose was not valued in summarizing a finding.

Even more influential to prioritizing automating compliance, reporting, and content production is that these white-collar professionals can pivot to other industries where their writing skills are valued.

The politically sensitive group is the billable consultants. But the reality is that if three associates plus an AI tool produce what ten associates used to produce, the firm only needs three associates [16] . When multiplied across hundreds of engagements and tens of thousands of staff, that is the source of the layoff math playing out across the industry through Q1 2026.

Where the Pyramid Pressure Is Heading

Cognizant reported Q1 2026 results on April 29, 2026, with seven large deals signed in the quarter and over 70% large-deal total contract value growth year-over-year [17]. CEO Ravi Kumar S framed the AI Velocity Gap (the distance between AI investment and tangible business outcomes) as the company's structural opportunity. The narrative is consistent across the implementation-led firms: the work clients want done has shifted from advice to delivery, and the talent profile is shifting with it.

Implication for Consultants

The pyramid model, where a large group of junior consultants drives consulting engagement, is over. The diamond shape of the consulting engagement is a reality now, where a traditional progression from analyst to manager to partner doesn't exist.

For mid-career consultants, that means the competition has halved, but so has the steepness to reach the next role.

AI agents with unlimited time and no emotions has no competition in a human sense but they are competing with you.

The leadership experience has been limited as there are fewer juniors to manage.

Orchestration and Governance skills are the bare minimum for consultants across the organizational hierarchy.

If you are working in large organizations:

1) Practice stakeholder persuasion and selling ideas to senior team members: These skills were relevant before AI, but matter even more now.

2) Build a public domain capability: The new Leaders tier (Deloitte) and equivalent layers at MBB are filled by consultants who have visibly owned a domain capability across engagements. Publish, present, or lead an internal capability build before the next promotion cycle.

3) Build an Individual Brand: There is a secret that anyone working for themselves knows from 2010: build a personal brand. That is the only thing that matters in a digital world. Don't be an influencer, but be a subject matter expert who can intelligently talk about the latest events and developments in consulting. Add credibility to your work through certification. Network aggressively to expand the reach of your message. The traditional partnership pathway in the consulting industry is dead.

For the Aspiring Consulting Applicant

One development we have seen consistently during an economic downturn or an industry disruption is the quick pivot to escape the pain in the labor market. You will have less competition in the consulting industry.

Former consultants have pivoted to government, investment banking, or frontier AI labs to train the next generation of AI models.

Prioritize firms that have accepted the reality of the new consulting hierarchy, like Deloitte.

The leader tier in Deloitte is a classic example of where the consulting industry is heading.

Right from the start, you are expected to learn and absorb client management, regulatory maneuvers, agentic AI fleet management, and an accountability that was unseen a few years back.

If you are targeting an MBA program, look deeply into leadership development opportunities.

Choose the most chaotic path where your time needs to be rationed. That is a much closer reflection of your life as a consultant.

Join 2-3 student clubs, opt in for exchange programs, volunteer for a non-profit that takes 5-6 hours of your time every week, while also targeting to feature on the Dean's list.

Time management will be the single biggest differentiator that you must test with an MBA.

Finally, forget about choosing one Consulting company as your destination.

Mention it in the MBA goals essay, but build optionality across consulting, AI lab joint ventures, and technology roles where you will be an orchestrator of AI agents and offer strategic guidance for the team.

The era of 'general management' skills is limited in the next 2-3 years. It will make a comeback in 5-6 years, but till then, prioritize technical and AI skills.

Don't choose MBA programs that are stubborn and stick to traditional case preparation with very little real-world AI integration experience.

If your goal is to succeed in consulting, ignore the M7 and HSW brand recall or ranking within them. Prioritize the curriculum first within M7 and HSW before shortlisting your dream MBA program.

Trend #4: Outcome-Based Pricing Becomes the Procurement Default

| Firm (Reporting Period) | Revenue | Bookings (Quarter) | Consulting / Services Segment | AI Disclosure | Headcount (approx.) |

|---|---|---|---|---|---|

| Accenture (Q2 FY26, ended Feb 28, 2026) [4] | $18.0B (+8% USD, +4% LC) | $22.1B record (Consulting $11.33B, Managed Services $10.78B) | Consulting $8.9B (+3% LC) Managed Services $9.2B (+5% LC) | 85,000+ AI & data professionals; on track to more than double bookings from key AI/data ecosystem partners vs FY25 | 801,000 |

| IBM (Q1 2026, ended Mar 31, 2026) [46] | $15.9B (+9% USD, +6% LC) | Not disclosed quarterly; $30B+ annualized consulting backlog | Consulting $5.27B (+4% USD, +1% LC) Strategy & Technology +1% LC Intelligent Operations +1% LC | watsonx Orchestrate the model-agnostic governance platform; clients orchestrating, deploying and governing AI across hybrid environments named as the growth tailwind | 270,000 |

| Cognizant (Q1 2026, ended Mar 31, 2026) [17] | $5.41B (+5.8% USD, +3.9% CC) | 21% YoY growth; 7 large deals ≥$100M, 1 mega deal ≥$500M; 70% growth in large-deal TCV; TTM bookings $29.6B (+11%) | Financial Services +12% YoY; Health Sciences +6.5%; Communications/Media/Tech +9.4%; Products & Resources +0.6% | Over 5,000 AI engagements; nearly 40% of code AI-assisted; "AI Velocity Gap" positioning; Project Leap restructuring announced | 357,600 (+21,300 YoY) |

| Capgemini (Q1 2026, ended Mar 31, 2026) [47] | €5.94B (+7% current, +11% constant currency) | €6.05B (+6.2% CC); book-to-bill 1.02 | North America +20.7% CC (29% of Group revenue); UK strong; France -1% | Generative and agentic AI bookings >11% of total Q1 bookings; WNS and Cloud4C acquisitions added 4.5-5 points inorganic growth; 5-year extension of McDonald's partnership | 421,000 (+78,300 YoY) |

| Big Four Private Disclosure (Fiscal year context) | Deloitte $69.2B FY25; PwC $55.4B FY25; EY $51.2B FY25; KPMG $40.4B FY25 | Not publicly disclosed | Audit, advisory and tax segments; advisory mix rising via AI engagements | Deloitte $3B GenAI through FY30; EY $1.4B (completed 2023); PwC OpenAI's largest enterprise customer at 200,000 ChatPwC seats; KPMG ISO/IEC 42001 first claim | Deloitte 460,000; PwC 370,000; EY 400,000; KPMG 275,000 (global) |

| MBB Private Disclosure (Calendar year 2025 estimates) | McKinsey $16B (2024 base); BCG $14.4B (2025); Bain $8B (estimated) | Not publicly disclosed | Strategy advisory dominant; implementation work growing | BCG: 25% of 2025 revenue ($3.6B) from AI work; McKinsey: 40% of projects AI-related, 20,000 AI agents alongside 40,000 humans; Bain: 19,000+ custom GPTs | McKinsey 40,000; BCG 33,000; Bain 19,000 |

| LC = Local Currency. CC = Constant Currency. TCV = Total Contract Value. TTM = Trailing Twelve Months. Private firms (Big Four, MBB) disclose annual but not quarterly figures; estimates are public-press cited. | |||||

Value-Based or Outcome-driven Pricing

For years, the consulting industry had mastered the hourly billing protocol where the 'decks' themselves took a quarter of the billing for a small engagement. But in Q1 2026, clients pivoted hard, now demanding value-based or outcome-driven pricing.

73% of clients preferred the new model, from which 58% [2] now discuss pricing in the initial discovery call itself.

For a reputed consulting firm, the conversation on pricing was delayed until scoping.

- The delivery time has shortened: From weeks, now an AI tool can deliver the same quality that a junior team member can provide. Clients, who themselves have used AI for productivity gain, now refuse to pay for weeks of labor that takes AI a few hours to do.

- Federal procurement: A side effect of Elon Musk's DOGE intervention is the direction in which Federal procurement has permanently changed in Q1 2026. In the General Services Administration (GSA) concessions package, where consulting giants had to justify their billing, performance-based fees were offered explicitly to retain contracts [1].

- EY first to price SaaS-style outcome contracts in client work: EY's February 17, 2026, publication on outcome-based pricing under ASC 606 outlines the revenue recognition mechanics for arrangements where the customer pays only for successful AI interactions [18] . These interactions don't require any Human-in-the-loop

McKinsey's Partner Compensation Pivot

Another affirmative action, as published in The Financial Times in May 2026, is McKinsey's plan to shift a greater proportion of partner remuneration into equity, with the explicit rationale that AI and outcome-based pricing make consulting revenues more volatile [8] .

For an asset-light partnership that historically distributed cash aggressively, if firms only get full payment once outcomes are achieved, payment cycles extend, and revenue becomes less predictable.

The first casualty will be variable pay and the increase in base salary in the consulting industry.

The Accenture Q2 FY26 Pricing Datapoint

Inside the March 19, 2026, results, two numbers framed where Accenture sits on the pricing transition [4]:

- Consulting new bookings: $11.33 billion

- Managed Services new bookings: $10.78 billion

- Consulting revenue: $8.9 billion, up 3% in local currency

- Managed Services revenue: $9.2 billion, up 5% in local currency

Managed Services growing faster than Consulting is an accurate reflection of what is happening in the Consulting industry.

Traditional Consulting roles in strategy, advisory, and project-based work have become more efficient due to agentic AI, orchestration platforms, and outcome-based pricing. Clients don’t need large teams and projects with large timelines.

Managed Services, which need ongoing maintenance, especially where transformational goals are closely tied to stock prices, clients want someone else to run the AI systems which works towards achieving the same strategic goals.

Historically, Managed Services contracts are planned around outcome and utilization economics.

Implication for Consultants

Outcome-based pricing changed everything in an engagement. Small hiccups in the project ecosystem outside a consultant's scope now need careful examination as they could impact the outcome of the deliverable.

From a general advisor, consultants must learn to manage risks and define KPI that matter to clients and are measurable for consulting companies.

The old days of disconnecting oneself from the firm's working capital management and limiting oneself to the scope of the consulting engagement is over. Now, everything is interconnected.

Revenue recognition and the pressure on working capital are also important metrics while suggesting deliverables for clients.

McKinsey's pivot to equity-based compensation will also limit a consultant's exploratory streak to investment banking or peer consulting companies.

Long tenure will be expected to reach financial equilibrium.

Build outcome-design literacy: The toughest variable to control is all outside the scope of the consulting engagement. The weakest links in a client's interaction could jeopardize the entire project. Creating a KPI verification mechanism is the first step to control outcomes.

One factor that a consultant can control is the depth of knowledge. The 25-40% healthcare knowledge premium and 20-35% financial services expertise premium documented in Q1 2026 are real and durable.

Consultants who add a sector credential (CFA, FRM, CPHIMS, CSCP) to their MBA outperform generalists on outcome-based engagement assignments.

From a compensation perspective, negotiating offers with calculation on the upside of equity stake can beat pure cash-based bonuses. But to think in this new way, one has to put on an entrepreneur's mindset and invest for the long-term in the consulting firm. In return for the loyalty, negotiate part of the funding for MBA programs.

For the Aspiring Consulting Applicant

For aspiring consultants, you don't have to reinvent the wheel. The Bain Net Promoter System, the BCG outcome-pricing playbook, and the McKinsey Implementation Quotient framework are outcome-based frameworks already publicly documented. Study and understand that all three frameworks value real economic impact over vanity metrics and systematic listening. Unlike the perception around Jargons and consultants, the three frameworks value simplicity & feedback loop to course correct.

Build a measurable accomplishment in a current role and learn to articulate it in outcome terms: Pre-MBA candidates who can describe their pre-MBA work in outcome language (revenue increase, cost reduction, timeline efficiency, with measurement methodology) outperform candidates who describe the same work in activity terms.

MBA resume’s 1-page format forces everyone to think in terms of IMPACT.

Even if the boom in AI might not maintain the same momentum in 2-3 years, and the technology industry would no longer retain the shine of the previous decades, healthcare, financial services, supply chain, and energy - four regulated industries would continue to attract consultants with 25-40% premium compensation is in these four industries.

Prioritize MBA programs that offer exposure to these four industries through club leadership, experiential learning, and summer internships.

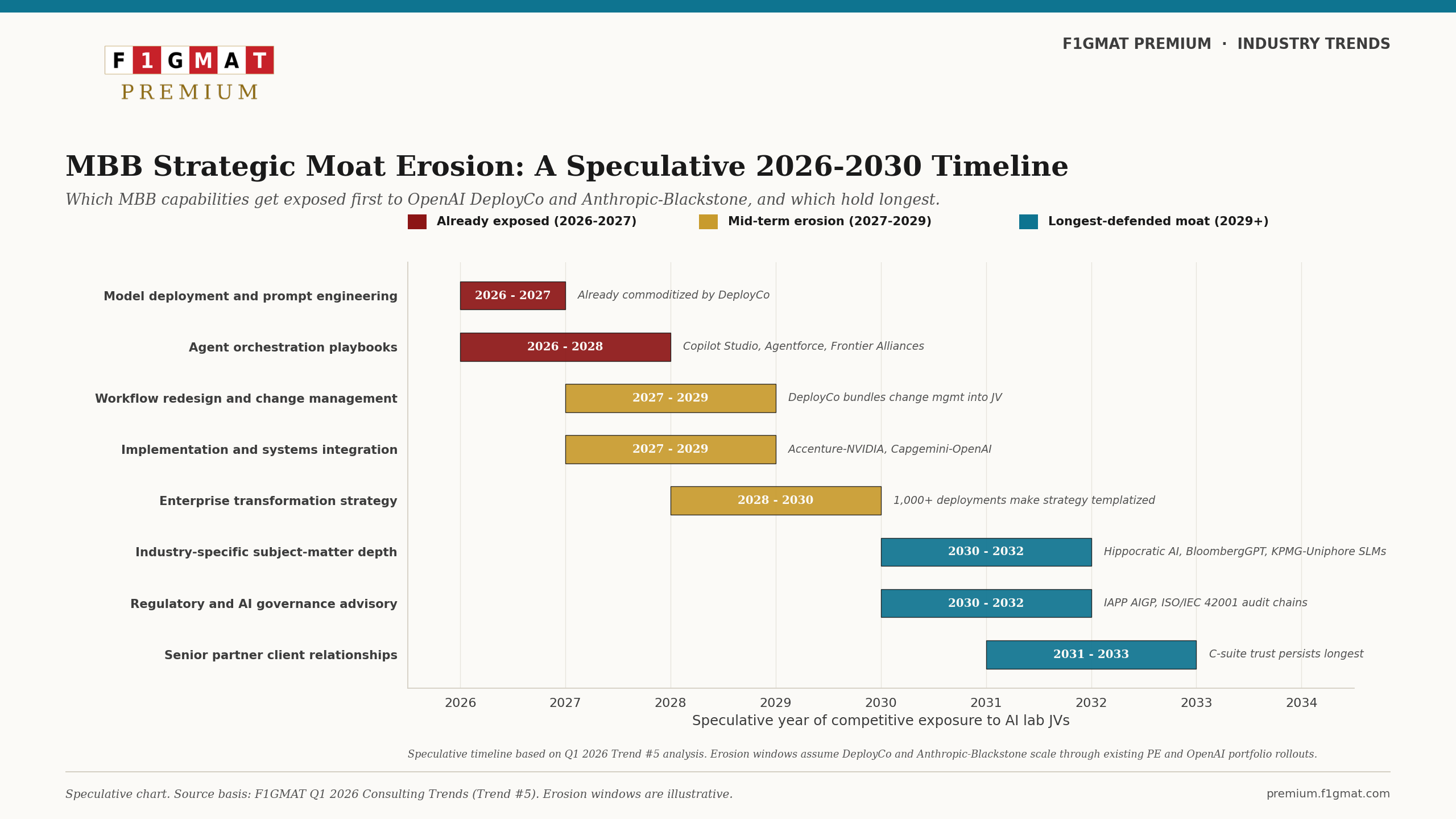

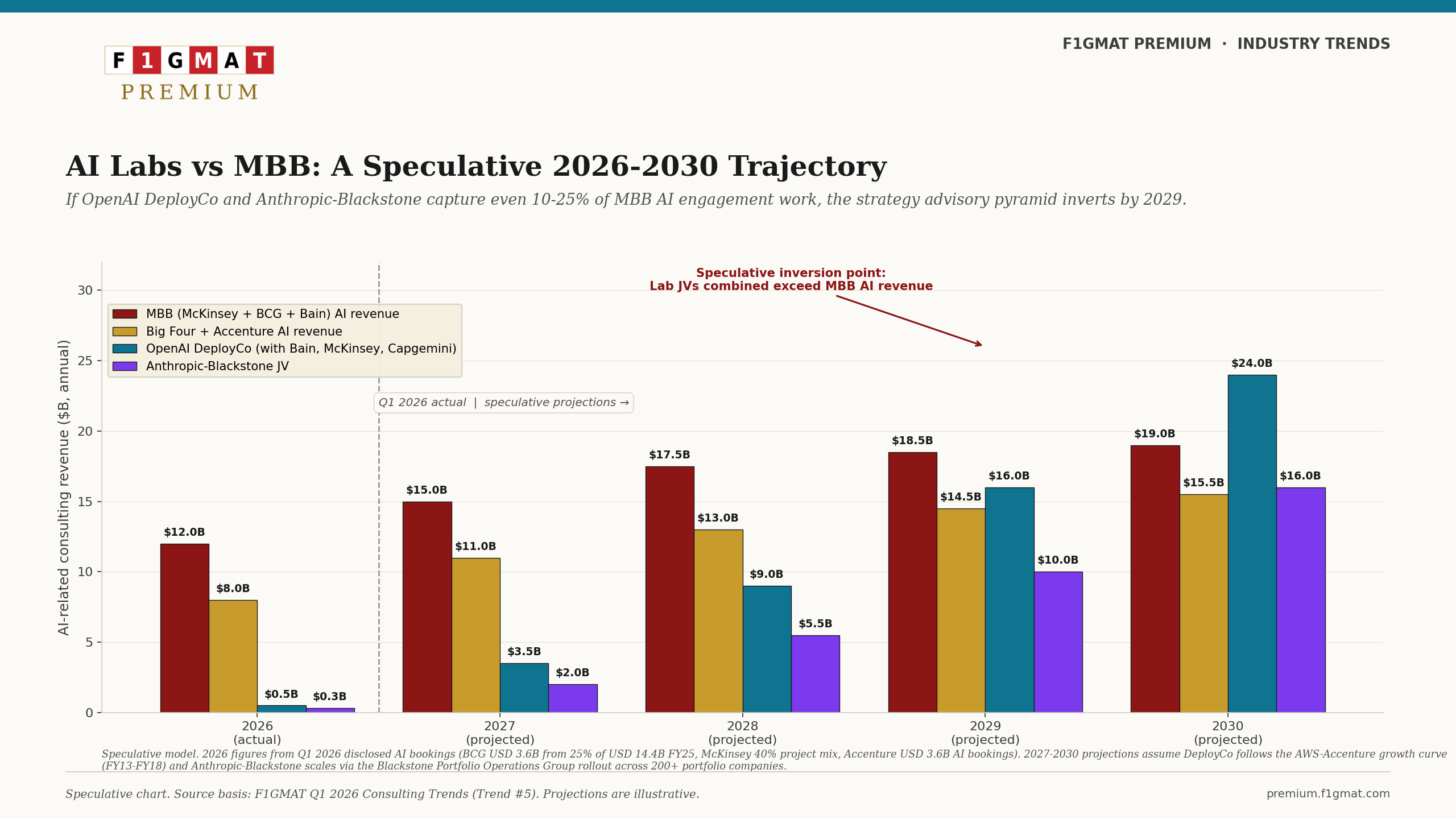

Trend #5: Frontier Labs and the Threat to the Big Three

OpenAI Frontier Alliances

In February 2026, OpenAI announced Frontier Alliances, naming McKinsey (via QuantumBlack), BCG (via BCG X), Accenture, and Capgemini as strategic implementation partners for Frontier, OpenAI's enterprise platform for AI coworkers [19] .

The four firms cover strategy definition, workflow redesign, system integration, and change management.

OpenAI is slowly recognizing that model innovation and tailoring products to enterprise vs. retail customers is not enough.

Teaming up with Consulting giants is one surefire way to stabilize revenue leaks caused by subscription cancellations in retail markets where users switch loyalty based on the potency of AI models.

Anthropic Builds the Partner Ecosystem

On February 16, 2026, in Bengaluru, Dario Amodei opened Anthropic's Builder Summit, the first major regional partner event [20] .

In parallel, Anthropic announced a $100 million investment in building a partner network. Anthropic also entered discussions with private-equity firms (Blackstone and Hellman & Friedman) about a structured distribution channel for Claude across portfolio companies.

The Risk The Big Three Faces

BCG reported in early 2026 that 25% of its $14.4 billion 2025 revenue (approximately $3.6 billion) came from AI-related consulting work [21]. McKinsey states that about 40% of its projects are now AI-related. Accenture reported $3.6 billion in AI bookings in 2025 with over 70,000 AI professionals. The AI slice of the consulting pie has crossed the threshold and determines firm-level growth and partner-level economics.

This is the slice that the frontier labs driven by AI companies are now positioning to participate in directly.

The AI giants need consulting partners for delivery, but the consulting partners now need the AI giants to retain client projects.

Once clients standardize on a model vendor, the delivery firm that comes with the model will win the strategy work.

The risk is in a scenario where, once the clients experience the efficiency gains and familiarity with the model, what stops the clients from hiring the AI firms directly and cutting off the consulting middlemen?

Q1 2026 Platform Race – Summary

Each firm's flagship platform has positioned itself for an ideal market in Q1 2026 [22]:

- McKinsey: Agents-at-Scale, Lilli (internal knowledge platform)

- BCG: BCG X, GENE (proprietary AI chatbot built on GPT-4o, now powering 6,000+ employee-built agents)

- Bain: Sage (proprietary AI chatbot), 19,000+ custom GPTs (strong OpenAI partnership)

- PwC: ChatPwC (approximately 200,000 internal users), Agent OS

- Deloitte: Zora AI (agentic model powered by NVIDIA), $3 billion GenAI investment through FY2030

- KPMG: Workbench, AI Pulse research, KPMG-Uniphore alliance for industry-specific small language models

- Accenture: AI Refinery, approximately 77,000 AI professionals, $3 billion AI investment

- EY: EY.ai platform, EYQ internal LLM, $1.4 billion AI investment completed in 2023

- Capgemini: Google Cloud partnership tilt, sector-specific integration

- IBM: watsonx, model-agnostic delivery with toggleable models

The Cost Advantage for Mid-Tier Firms

Right now, mid-tier firms are struggling to compete with the big consulting firms because the industry is in flux.

Even Microsoft, which leads the orchestration layer, is only ahead by 13 points. There is no clear market leadership or monopoly in the space. Without market leadership, it is costly for mid-tier firms to train and certify their consultants on multiple vendors.

Once AI leadership is established at an enterprise level, picking an alliance for enterprise, developer tooling, and workflows could be achieved at a faster pace. Then, pricing a consultant at a lower hourly rate could be justified when large consulting firms would have adopted an outcome-based pricing.

Implication for Consultants

Each consulting firm has picked its AI partner.

McKinsey has chosen Microsoft Copilot Studio and Azure AI.

BCG consultants benefit from Anthropic Builder credentials.

Deloitte consultants benefit from NVIDIA AI Enterprise certification.

Prioritize the preferred partner in your organization to increase the likelihood of attracting higher billing.

Even though prioritizing partners is the first step, markets can change. Vendors can evolve and lose market share. Maintain at least one secondary platform exposure.

A McKinsey consultant with Microsoft depth plus exposure to Anthropic carries optionality if the engagement mix changes.

The most important development in Q1 2026 is the advent of AI Lab and Consulting Joint ventures.

OpenAI's DeployCo and the Anthropic-Blackstone JV are positioned to compete with consulting firms in the long-term.

Consultants whose engagement work falls inside the DeployCo or Anthropic-Blackstone target zone should expect competitive pressure, within the AI Lab and Consulting ecosystem, in addition to competition from peers from other consulting giants.

For the Aspiring Consulting Applicant

Instead of choosing firms based on the AI partner, prioritize the industry.

Ask any technology industry veteran what happened to their product-specific expertise. They all became redundant.

The only thing that remained were their programming skills.

In consulting, industry expertise is the Moat.

If your long-term career interest is in healthcare or financial services, acquire AI tool proficiency in Hippocratic AI.

If you want to be part of the enterprise transformation team, prioritize Zora AI on NVIDIA.

Choose the AI tools integrated in an industry. These are all tools. Eventually, your subject matter expertise in an industry is valued the most.

Having said that, in the short-term until the AI race settles, build pre-MBA credentials in Microsoft AI-102, Anthropic Builder, NVIDIA AI Enterprise, or Google Cloud AI Engineer. It takes 4-8 weeks of structured study to master these certifications.

Show the early commitment before completing pre-MBA foundational courses.

Another development you must anticipate is the incursion of OpenAI's DeployCo and Anthropic-Blackstone partnership to disrupt the competitive compensation in MBB.

Applicants who limit their target list to traditional consulting firms in 2026-2028 may be ignoring the highest-growth option available post-MBA. Keep an open mind.

Trend #6: EU AI Act Drives Compliance Demand

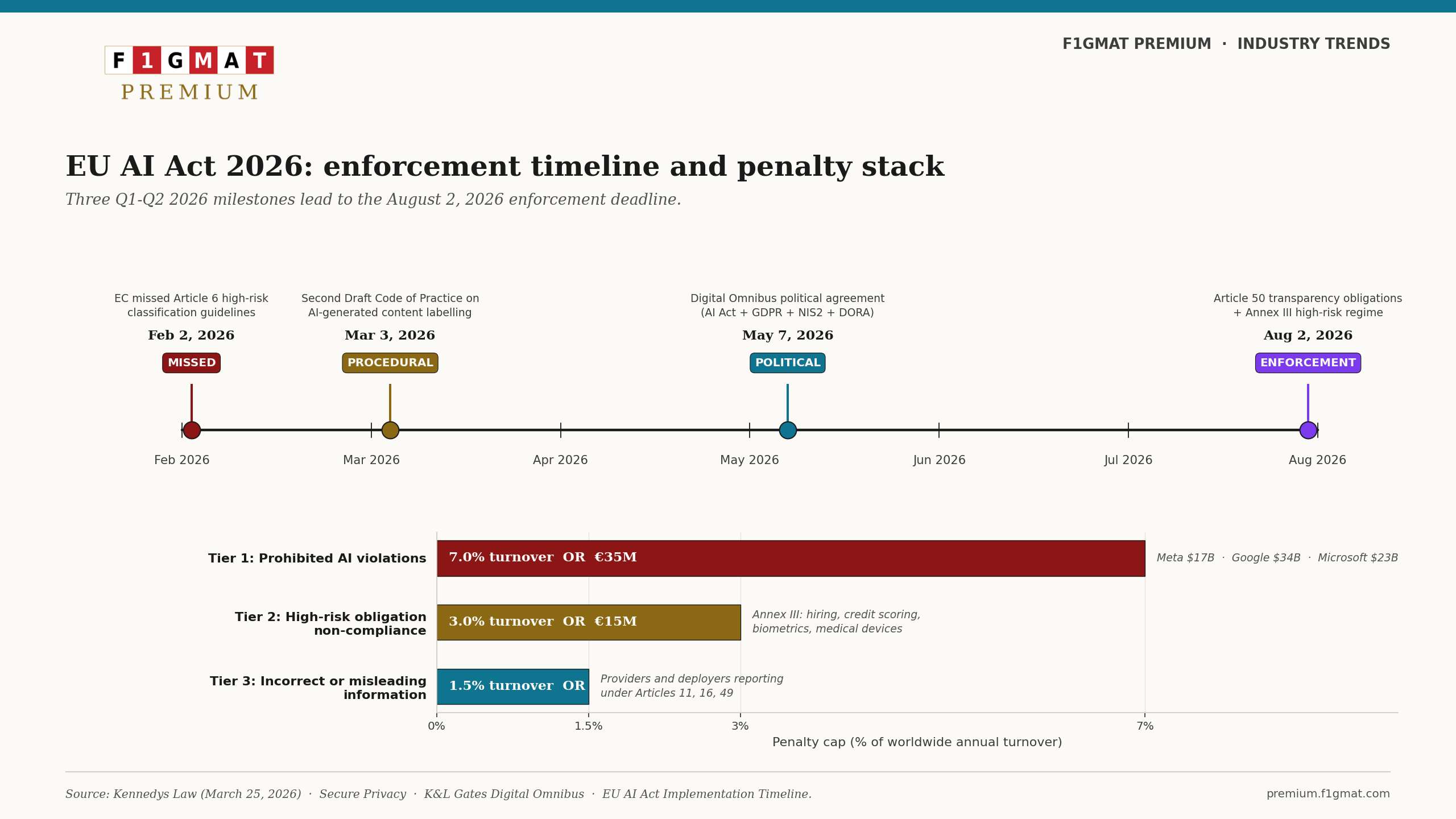

The EU AI Act

Two AI Act milestones fell inside Q1 2026 [23] :

- February 2, 2026: The European Commission missed the statutory deadline of February 2, 2026, for issuing detailed guidelines on the practical implementation of Article 6, which covers classification rules for high-risk AI systems and a comprehensive list of practical examples. The Article was supposed to cover Annex III use cases in employment, education, credit scoring, biometric identification, and critical infrastructure

- March 3, 2026: The Second Draft Code of Practice on marking and labeling of AI-generated content was published. The code is a precedent on how conversation agents will interact with tools in Enterprise platforms and specialist agents in the ecosystem. The code was mostly on technical and operational steps for marking, watermarking, labeling, and detecting AI-generated content.

August 2, 2026, is the final deadline when the majority of remaining AI Act rules become enforceable. From procedural steps on March 3, 2026, the release should include the missed February 2, 2026, guideline on transparency obligations under Article 50 and the high-risk AI system regime under Annex III [23] .

The Penalty

The EU AI Act establishes a three-tier penalty regime [24]:

- Prohibited AI violations: up to €35 million or 7% of the total worldwide annual turnover, whichever is higher

- Non-compliance with high-risk obligations: up to €15 million or 3% of total worldwide annual turnover

- Incorrect or misleading information: up to €7.5 million or 1.5% of the total worldwide annual turnover

For context on the scale of the penalty, 7% of global revenue would cost Meta approximately $16-17.5 billion, Google approximately $34 billion, and Microsoft approximately $23 billion based on projected 2026 financials.

The Digital Omnibus

The European Commission's Digital Omnibus proposal (adopted November 19, 2025, with political agreement reached on May 7, 2026) consolidated AI Act amendments with GDPR, NIS2, DORA, and the Data Act [25] .

Where Consulting Demand Sits

- AI inventory and classification (catalog every AI system, including third-party tools and embedded features) [26]

Most large organizations have hundreds or thousands of AI uses scattered across departments. Consultants help build AI registries, classify each system (prohibited, high-risk, limited-risk, or minimal-risk), and maintain them on an ongoing basis.

- Gap analysis and risk assessment for high-risk systems [26]

91% of leaders say data security, privacy, and risk will influence AI strategies over the next six months [10] . Many companies are discovering they have far more high-risk systems than expected (e.g., in hiring, credit scoring, medical devices, insurance pricing). Consultants are heavily engaged in risk scoring and remediation roadmaps.

- Technical documentation

Creating comprehensive technical files for each high-risk AI system, including design specs, training data details, testing results, and ongoing monitoring plans is the most cumbersome and useful part of the consulting engagement.

- Conformity assessment readiness and CE marking strategy

For any products sold in the EU, there is a mandatory conformity mark required for many products (and now certain AI systems) before they can be legally placed on the EU market or put into service in the European Economic Area (EEA).

Preparing for the formal conformity assessment process (internal or via Notified Bodies) and developing a strategy for CE marking (Conformité Européenne) on high-risk AI systems covers validation protocols, quality management systems, and post-market surveillance plans, which occupied the consultants' time the most in Q1 2026.

- Cross-framework integration (AI Act, GDPR, DORA, NIS2)

Because building separate compliance programs for each law is expensive, clients expect consultants to offer a layered approach, where regulations are layered on top of each other. In Q1 2026, this is one of the highest-value consulting engagements because it requires deep expertise across legal, technical, risk, and operational teams.

Implication for Consultants

The EU AI Act compliance is the fastest-growing engagement category at every major firm in Q1 2026.

Consultants currently placed on European client accounts (or US client accounts with European operations) carry a structural assignment advantage through August 2, 2026, and beyond.

The compliance work does not end at the enforcement date; the audit, monitoring, and incident-response work continues indefinitely. This is the closest analog to GDPR compliance work in 2018-2020 that consulting firms have seen, and it represents a multi-year billable engagement pipeline.

Two priorities for the consultant in 2026:

1) Acquire the IAPP AIGP (AI Governance Professional) credential in the next 12 months. The certification is now the closest the industry has to a standard credential for AI compliance work, and recruiters at every regulated-vertical client now request it explicitly in the engagement team profile.

2) Complement AI Act compliance with proficiency in adjacent frameworks (GDPR, DORA, NIS2). Cross-framework integration is the most under-served engagement type and contributes to cost savings in client companies. Prioritize frameworks with regulatory overlap like GDPR Article 22 automated-decision provisions intersect with AI Act Article 14 human oversight requirements.

For the Aspiring Consulting Applicant

AI governance and compliance is the fastest-growing AI-adjacent role category by hiring velocity. IAPP's AI Governance Profession Report finds 77% of organizations are actively building AI governance programs (climbing above 85% at companies already deploying AI), and only 1.5% report being satisfied with their current governance headcount. The supply-demand imbalance creates the strongest entry-point dynamic in AI consulting in 2026-2028.

Acquire the IAPP AIGP credential during the MBA. The certification carries strong recognition at Big Four advisory, MBB regulated-vertical practices, and large financial services firms.

The 60-80 hour study commitment fits inside a single MBA semester and shows capability in a market where most candidates have only general AI awareness.

Another strategy is to target firms with disclosed AI governance expertise like KPMG's ISO/IEC 42001, in addition to a partnership with Uniphore SLM, EY's $1.4 billion AI investment with explicit governance focus, and Deloitte's Zora AI and the Trustworthy AI framework, and even PwC's integrated Responsible AI practices.

To build compliance expertise while also building general management and leadership skills, prioritize MBA programs in universities with strong law programs like Penn (Wharton and Penn Law), Yale (SOM and Yale Law), Northwestern (Kellogg and Pritzker), and Georgetown (McDonough and Georgetown Law). If you want to super-specialize in the regulatory track, choose joint JD-MBA tracks.

While expertise in regulatory laws is a good starting point, in a fragile global supply chain, cross-jurisdictional capability is even more important.

The 2027-2028 governance consultant will be expected to advise on the AI Act, US state-level regulation (Colorado SB 24-205, California SB 53), India DPDP, and China PIPL simultaneously.

Applicants who build awareness of all four frameworks during the MBA are positioned for the multi-jurisdictional engagements that carry the highest rates.

Trend #7: Trade Advisory Becomes a Strategic Core Practice

The IEEPA Catalyst

The February 20, 2026, Supreme Court ruling on the IEEPA created the largest single-event trade advisory demand pulse of Q1 2026 [7]. Deloitte's own client communication noted that more than 70% of respondents in a recent Dbriefs webcast had not started initial tariff modeling and assessment work [7].

Auto Tariffs and the USMCA Inflection Opportunities

Automotive tariffs are set at 15% to 20%, with country-specific exceptions [28]. Mexico and Canada have practical relief on many items through USMCA, but the 2026 USMCA review is a near-term shock that could rewrite the entire North American supply chain economics. For automotive clients, this has driven trade and tariff exposure modeling and M&A advisory for the supply chain restructuring that follows [29] .

The Macroeconomic Drag

The re-evaluation of the supply chain economics will impact Mexico, Canada, and China, which indirectly will cut American disposable income by 1% in 2026 [28].

The 1% average doesn't evenly play out. For households, the effect is changing the budget from discretionary and consume goods spending to mobility budget in cars or trucks. Consultants must evaluate the impact of such budget relocation on the demand for clients .

The demand dip should be addressed with appropriate SKUs and promotional strategies. Even capex changes are driven by an accurate forecast of these supply chain dynamics.

The Big Four Tariff Race

Deloitte and EY have uniquely positioned themselves for Tariff-led trade disruptions, with the former adopting a comprehensive toolkit and the latter with a strategic consolidation.

Deloitte's Q1 2026 client-facing toolkit includes Tariff Vision (a proprietary tariff exposure quantification tool integrated with Global Trade Advisory Services), Supply Chain Intelligence (a digital platform integrating legal entity data, financial metrics, and transactional flows), and SupplyHorizon N-tier ( AI-powered N-tier supplier mapping ) [30] .

While digital platform was not the go-to strategy for EY, the firm's January 2025 expansion of EY-Parthenon to a 25,000-person strategy and transactions practice, including M&A advisory, real estate advisory, and restructuring teams, paid off in Q1 2026 as trade-driven restructuring became the dominant transaction type [31] for the niche.

Where the Engagement Profile Is Going

Tariff advisory has become a “must-have” entry ticket for any consulting firm that wants to win and retain meaningful work with manufacturing, industrials, automotive, chemicals, energy, and supply-chain-heavy clients in 2026.

In Q1 2026, Trade advisory is its own separate service outside taxation and spans: Tariff exposure quantification, Supplier sub-tier visibility (N-tier mapping), pricing realignment, Operational footprint redesign (nearshoring, reshoring, in-country production), M&A advisory for tariff-driven supply chain consolidation, and financial impact assessment and scenario modeling for tariff outcomes.

If consultants can’t credibly lead the tariff discussion, they don’t get invited to the much larger, multi-year operating model transformation project.

Implication for Consultants

Trade advisory has moved from a niche tax specialty to a core practice across every major firm in Q1 2026.

Consultants currently in supply chain, operations, M&A advisory, or strategy practices that touch manufacturing, industrials, automotive, or consumer goods clients face an immediate skill expansion .

The senior partner running an industrials portfolio now expects every team member to discuss HTS codes, USMCA eligibility, and N-tier supplier mapping in client meetings.

Consultants who cannot have this conversation are removed from staffing decisions for trade-affected engagements.

A lot of the trade advisory vocabulary can be learned at your own pace in 30 to 60 days by reading Deloitte's Tariff Vision documentation, McKinsey trade advisory publications, and the USTR public framework. Prioritize concepts in HTS classification, country-of-origin rules, Free Trade Agreement eligibility, transfer pricing for customs valuation, and N-tier mapping methodology.

Even more valuable than learning concepts is a lateral move to trade-affected portfolios.

Consumer goods, automotive, semiconductors, pharma, and industrial manufacturing are five niches where most consulting opportunities are right now. These moves need some adjacent industry exposure in operations, supply chain, and M&A.

To sell your fit for the lateral move, acquire one trade credential.

The CCS (Customs Compliance Specialist) certification, the Licensed Customs Broker exam, or the ASCM CSCP credential are three exams worth prioritizing. The 6-12 week investment could easily support consulting opportunities for the next 2-3 years until the republicans are not in the office or when American foreign trade policy pivots back to the demo cratic norms.

For the Aspiring Consulting Applicant

Target firms with disclosed trade advisory platform investments like Deloitte's Tariff Vision, Supply Chain Intelligence, and SupplyHorizon N-tier.

Even the consolidation of teams like EY-Parthenon's January 2025 expansion to a 25,000-person team with deep expertise in strategy is a sign of positioning for the market demand.

The safest bets are in targeting consulting firms with specialized industry groups like PwC's Tariff Industry Group.

The second action item is to build USMCA and IEEPA fluency to explain the cascading effect of tariffs on pricing before the interview season.

If an MBA program is a near-term goal, choose programs with strong international business and supply chain depth.

Cornell SC Johnson, MIT Sloan (Center for Transportation and Logistics), Penn State Smeal, Michigan Ross (Tauber Institute), and the University of Tennessee Haslam offer the strongest supply chain expertise.

If you want an M7 MBA instead of compromising for Penn State, Michigan, or Cornell SC Johnson, choose programs where the summer internship is in a trade-affected sector.

Automotive, consumer goods, semiconductors, pharmaceuticals, and industrial manufacturing all carry strong trade advisory engagement opportunities.

For personal knowledge building, read the public outputs of the Office of the US Trade Representative (USTR), the Mexican Secretaria de Economia trade publications, and the European Commission DG Trade reports.

The cross-jurisdictional fluency that the 2027-2028 trade advisor needs starts with awareness of how each major economy frames its own trade policy.

References

- Big firms offer concessions in federal consulting crackdown (Consulting.us coverage of GSA letter and concessions package) ↩ ↩ ↩ ↩

- Consulting Rate Card (2026): Templates and Pricing Menu (Data-Mania, 2026 rate benchmarks) ↩ ↩

- Deloitte to scrap traditional job titles as AI ushers in a modernization of the Big Four (Fortune, January 22, 2026) ↩ ↩ ↩

- Accenture Reports Second-Quarter Fiscal 2026 Results (Accenture, March 19, 2026 press release and Form 8-K) ↩ ↩

- DOGE and US Government Cut At Least $1.5B In Consulting Spend (Management Consulted, with April 22 update on the $20B in additional cuts) ↩

- DOGE's private contract crackdown has eliminated more than 120 Deloitte contracts (Fortune analysis of DOGE filings) ↩

- Navigating Trade and Tariff Impacts (Deloitte US, referencing the February 20, 2026 Supreme Court IEEPA ruling) ↩ ↩ ↩

- Consulting's Partnership Model Is Shifting with AI (Strat-Bridge analysis of FT reporting on McKinsey partner remuneration shift) ↩ ↩

- AI Agent Adoption 2026: 120+ Enterprise Data Points (Digital Applied, compiled from Gartner, McKinsey, S&P Global, IDC, Forrester, BCG telemetry through April 2026) ↩ ↩

- KPMG US Q1 AI Quarterly Pulse: Investment and AI Agent Deployment Surge as Execution Becomes the Differentiator (KPMG, March 31, 2026) ↩ ↩

- Claude's next enterprise battle is not models: it's the agent control plane (VentureBeat, Q1 2026 VB Pulse Orchestration Tracker) ↩

- AI Agents in Production 2026: Orchestration, Governance, and Windows Enterprise Control (Windows News, May 2026). ↩

- 2026 Consulting's AI Revolution Update: Billions Spent, But the Old Pyramid Persists (Future of Consulting, January 25, 2026). ↩ ↩

- AI Influences How McKinsey, BCG, Bain Hire for Entry-Level Consulting Jobs (Bloomberg Businessweek, April 15, 2026 cover, reporting on Q1 2026 dynamics). ↩

- McKinsey, BCG & Bain Layoffs: Inside the Consulting Crisis (Case Interview Hub, April 2026). ↩

- McKinsey Layoffs 2026: 200 Jobs Cut as AI Reshapes Elite Consulting (Metaintro, 2026). ↩ ↩

- Cognizant Q1 2026 Results Press Release (Cognizant Form 8-K, April 29, 2026). ↩ ↩

- SaaS transformation with GenAI: outcome-based pricing (EY US, February 17, 2026 publication). ↩ ↩

- The AI Adoption Gap: What OpenAI and Anthropic Know (SoftSnow, on the OpenAI Frontier Alliances with McKinsey, BCG, Accenture, Capgemini). ↩

- Anthropic takes shot at consulting industry in joint venture with Wall Street giants (Fortune, on Anthropic Builder Summit Bengaluru, February 16, 2026 and partner network buildout). ↩

- BCG Rode AI to $3.6B in Revenue (Metaintro, 2026, on BCG's 25% AI revenue share of $14.4B 2025 total). ↩ ↩

- The Big Consulting AI Frameworks, Compared (2026) (Consulting Huber benchmark of BCG, McKinsey, Deloitte, EY, PwC, KPMG, Accenture, Bain, Capgemini, IBM). ↩ ↩ ↩ ↩ ↩ ↩ ↩

- The EU AI Act implementation timeline: understanding the next deadline for compliance (Kennedys Law, March 25, 2026). ↩ ↩

- EU AI Act 2026: Key Compliance Requirements for Enterprises (Secure Privacy, 2026 on Article 5 penalty structure). ↩

- EU and Luxembourg Update on the European Harmonised Rules on Artificial Intelligence (K&L Gates, January 20, 2026, on the November 2025 Digital Omnibus proposal). ↩

- EU AI Act 2026: Compliance Guide for European Businesses (Digital Applied, February 3, 2026, Q1-Q2 2026 compliance roadmap). ↩ ↩

- KPMG enters strategic relationship with Uniphore to build AI agents powered by industry-specific small language models (Uniphore press release). ↩

- Enhancing supply chain resilience in a new era of policy (Deloitte Insights, with Tax Foundation 2026 disposable income estimates and tariff impact analysis). ↩ ↩

- Tariffs Are Reshaping Auto Supply Chains and Creating M&A Opportunities (GlassRatner, December 17, 2025). ↩

- Tariffs, Trade, and Supply Chain Planning (Deloitte US, on Tariff Vision, Supply Chain Intelligence, and SupplyHorizon N-tier). ↩

- Big 4 Consulting Firms: Deloitte, PwC, EY & KPMG (2026) (RoadToOffer, on January 2025 EY-Parthenon expansion to 25,000-person practice). ↩ ↩

- Rewiring the way McKinsey works with Lilli, our generative AI platform (McKinsey & Company, 70%+ active usage and Lilli architecture detail). ↩

- How an AI Agent Hacked McKinsey's AI Platform (Outpost24, CodeWall disclosure of the March 9, 2026 Lilli breach). ↩

- BCG and Hippocratic AI Announce Strategic Collaboration to Deploy Agentic AI Across Biopharma and Medtech (BCG press release, January 8, 2026). ↩

- Why Generative AI is Reshaping Consulting (NorthStar Consulting UK, deployment data on Lilli, GENE, Deckster, Sidekick, Bain Copilot rollout). ↩

- OpenAI launches AI consulting arm valued at $14 billion (Axios, May 11, 2026, on DeployCo and Bain/McKinsey/Capgemini as partners). ↩

- Deloitte Begins Rollout of AI Agents for Finance and Other Business Functions (PYMNTS coverage of Zora AI, March 2025). ↩

- 2026 AI Business Predictions (PwC, on Agent OS and AI-led workflow automation thesis). ↩

- McKinsey Has 20,000 AI Agents: What It Means for Jobs 2026 (Vucense, March 2026, on 40K humans + 20K agents workforce mix and Lilli MCP integration). ↩

- Q4 2025 Consulting Trends (F1GMAT Premium, anchor source for the prior period). ↩

- Promoting Efficiency, Accountability, and Performance in Federal Contracting (White House Presidential Actions, April 2026). ↩

- EU AI Enforcement Act Timeline (Artificial Intelligence Act EU). ↩

- On-Premise vs Cloud: Generative AI Total Cost of Ownership (2026 Edition) ↩

- Head of Regulatory Affairs - Job Posting ↩

- The State of AI in the Enterprise

- IBM Releases First-Quarter 2026 Results ↩

- Capgemini Q1 2026 Revenues ↩